If income is charged as a part of the installment sale, income earned each tax year is taxed as ordinary income. If a business is being sold, the seller will use Form 4797, Sales of Business Property, instead.

Is an installment sale passive income?

Installment Sales – If you dispose of a passive activity in an installment sale, the suspended passive losses from the activity become available as the buyer makes payments. Losses become available in the same ratio that gain recognized each year bears to the total gain on the sale.

What are the requirements for an installment sale?

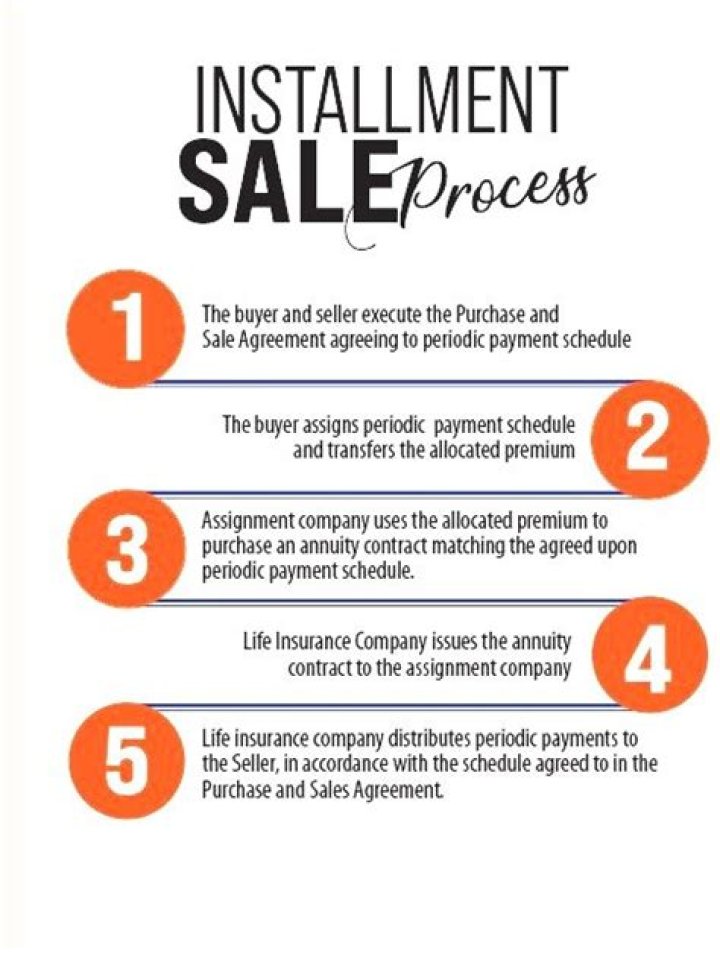

This tax strategy is known as an installment sale. Installment sales require two factors: You agree to sell an asset to a buyer with payments made over time. At least one payment must be received within a year after the tax year of the sale.

How are installment sales reported on a tax return?

You may elect out by reporting all the gain as income in the year of the sale on Form 4797, Sales of Business Property, or on Schedule D (Form 1040), Capital Gains and Losses and Form 8949, Sales and Other Dispositions of Capital Assets. Installment method rules don’t apply to sales that result in a loss.

How is an installment sale reported in SEC 453?

The entire $1,000 gain is eligible for installment sale reporting under Sec. 453. The realized gain on the asset sale is $1,000, but none of the gain is recognized. After the asset sale, the S corporation adopts a plan of liquidation and distributes the note in liquidation.

What happens to a S corporation during an installment sale?

Because no cash is received, the S corporation recognizes no gain, and the shareholder’s basis remains zero. Since the installment obligation is the only asset distributed in liquidation, the shareholder takes a zero basis in the receivable, and all payments received are taxable.