Accrual refers to an entry made in the books of accounts related to the recording of revenue or expense paid without any exchange of cash. Under the accrual method of accounting expenses are balanced with revenues on the income statement. It helps give a better picture of the company’s financial condition.

Can S Corp be accrual basis?

As an S corporation, you can use either the accrual or cash accounting method if you don’t keep an inventory. If you maintain an inventory, you have to use the accrual method. The IRS considers an inventory to be items you produce, purchase or sell to generate income.

Who can maintain books on cash basis?

But if you match one of the types of business structures listed below, you can use cash-basis accounting:

- You are a C corporation or partnership with average gross receipts of less than $5,000,000 per year.

- You are a sole proprietorship or an S corporation with average gross receipts of less than $1,000,000 per year.

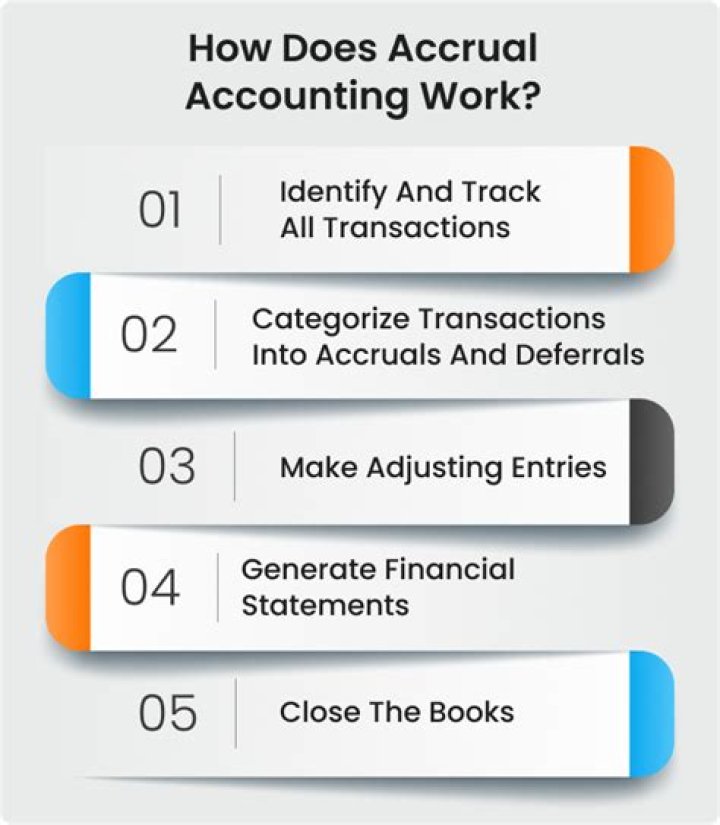

When does accrual accounting method record anticipated revenue?

The accrual accounting method records anticipated revenue when a product or service is delivered, even if payment for said-product has not yet been received. Expenses, too, are reported in the year they are incurred, regardless of when they will be paid.

How is book income reported to the IRS?

It is regulated by the laws in theInternal Revenue Code, (IRC) and accepts either cash, accrual or a hybrid as valid methods of reporting to determine how much of the company’s income is taxable. Book income describes a company’s financial income before taxes.

How does the cash basis method of accounting work?

The cash basis method of accounting involves an immediate recognition of revenue and expenses. Revenue is reported on the income statement only when money is received, and expenses are only recorded for the tax year when they are actually paid out.

Where do I find accrual accounting on my tax return?

This reconciliation is contained on Schedule M-1 on 1065, 1120 and 1120S returns. The accrual accounting method records anticipated revenue when a product or service is delivered, even if payment for said-product has not yet been received.