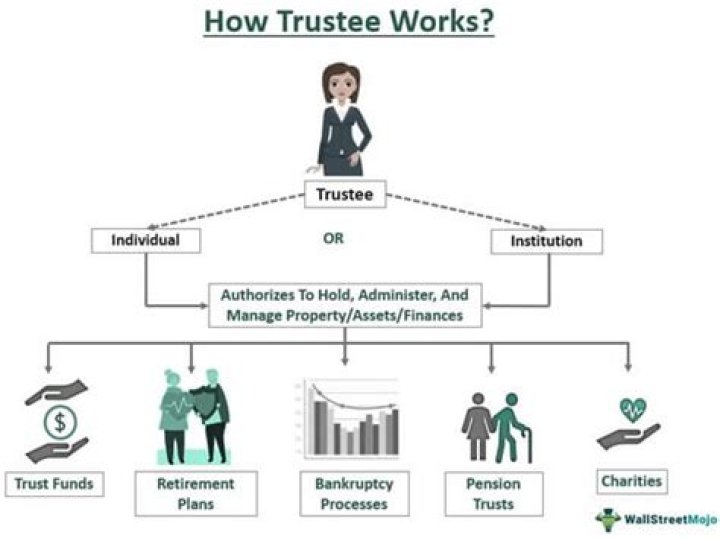

A trust might be created to provide legal protection for the assets of the trustor and to ensure that the assets are distributed properly. A trustee is thus responsible for the proper management of all property and other assets owned by the trust for the benefit of a beneficiary.

What are the benefits of setting up a trust?

5 potential benefits of setting up a trust

- Trusts avoid the probate process.

- Trusts may provide tax benefits.

- Trusts offer specific parameters for the use of your assets.

- Revocable trusts can help during illness or disability – not just death.

- Trusts allow for flexibility.

Is the trustee of a trust entitled to compensation?

Under California Probate Code section 15680, a trustee is entitled to be compensated as set forth in the instrument. Alternatively, the creators might set an hourly rate (perhaps indexed for inflation) that the trustee may charge. Even general language regarding the intent to pay a fee might help avoid a fight.

What is the role of a trustee in a trust?

A trustee is a person or company who manages the trust’s assets for the benefit of the beneficiaries. Their duties are set out in the trust deed. Trustees must not benefit personally from their role unless they hold the trust in a professional capacity and receive a fee for their service.

Who are the beneficiaries of a trust?

At its simplest, a trust is an arrangement whereby property or assets are transferred from one person (the ‘settlor’) to another person (the ‘trustee’) to hold the property for the benefit of a specified list or class of persons (the ‘beneficiaries’).

What are the advantages of a Trust Company?

The practical advantages of a trust are gained from the distinction that is drawn between the formal or legal owner of property, the trustee, and those people that have the use or benefit of the property, the beneficiaries. It is vital that the trustee remains independent and exercises proper control over the trust property.

What are the benefits of a family trust?

Benefits of a family trust. Family trusts are designed to protect our assets and benefit members of our family beyond our lifetime. When our assets are in a family trust we no longer have legal ownership of them – the assets are owned by the trustees, for the benefit of our family members.