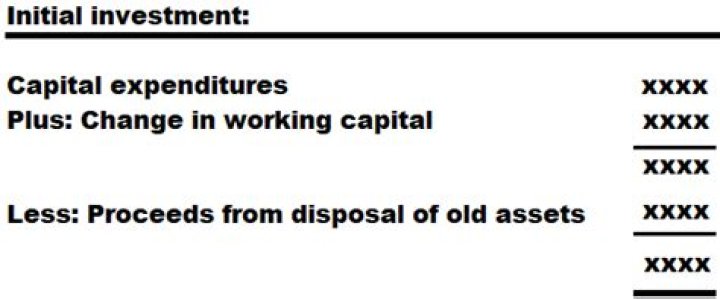

Formula. Initial investment equals capital expenditures or fixed capital investment (such as machinery, tools, shipment and installation, more) plus a change in working capital, minus proceed from the sale old asset, plus tax adjusted profit or loss from the sale of assets.

How do you calculate capital budgeting?

Preparing a Capital Budgeting Analysis

- Step 1: Determine the total amount of the investment.

- Step 2: Determine the cash flows the investment will return.

- Step 3: Determine the residual/terminal value.

- Step 4: Calculate the annual cash flows of the investment.

- Step 5: Calculate the NPV of the cash flows.

What is initial capital outlay?

An initial outlay refers to the initial investments needed in order to begin a given project. Nonetheless, they should also take into account the initial outlay of capital required to pursue the selected project, as well as which sources of capital they intend to draw upon.

What is initial investment value?

Initial investment is the amount required to start a business or a project. It is also called initial investment outlay or simply initial outlay. It equals capital expenditures plus working capital requirement plus after-tax proceeds from assets disposed off or available for use elsewhere.

What is an example of capital budget?

Capital budgeting makes decisions about the long-term investment of a company’s capital into operations. Planning the eventual returns on investments in machinery, real estate and new technology are all examples of capital budgeting.

Is working capital included in initial outlay?

This cost also encompasses installation and shipping costs involved with purchasing equipment. This is often considered to be a long-term investment. Working Capital. This part of the initial outlay is often considered to be a short-term investment.

How is initial cash outlay calculated?

To calculate the initial investment outlay, take the cost of new equipment for the project plus operating expenses such as supplies. Subtract the value of any old equipment you sell off, then add any capital gains tax or loss you make on the sale. That gives you your outlay.

How do you calculate initial investment?

Multiply the sum by the number of years in question. Take the future value you have in mind and divide it by that sum to find out the initial investment you need.

Do you include fixed costs in capital budgeting?

Capital Budgeting Example The initial investment includes outlays for buildings, equipment, and working capital. $110,000 of cash revenue is projected for each of the 10 years of the project. After variable and fixed cash expenses are subtracted, $50,000 of net cash flow (before taxes) is generated.

What is capital budgeting explain with practical examples?

Capital Budgeting primarily refers to the decision making process related to investment in long term projects, an example of which includes the capital budgeting process conducted by an organization in order to decide that whether to continue with the existing machinery or buy a new one in place of the old machinery.

What are the main criteria for capital budgeting valuation?

While net present value is the rule that always maximizes shareholder value, some firms use other criteria for their capital budgeting decisions, such as:

- Internal Rate of Return (IRR)

- Profitability Index.

- Payback Period.

- Return on Book Value.

How is capital outlay calculated?

To find the total capital outlay, add the total of the non-current tangible assets to the total of the non-current intangible assets. This the capital outlay for the specific accounting period indicated on your balance sheet. You can use previous balance sheets to learn about the depreciation of your assets.

What are the four capital budgeting criteria?

namely: 1) discounted payback period, 2) net present value, 3) modified rate of return, 4) profitability index, and 5) internal rate of return. We employ a unifying concept, cumulative present value (CPV), to highlight the commonalities among these criteria.

What are the three approaches to capital budgeting?

Capital budgeting is the process by which investors determine the value of a potential investment project. The three most common approaches to project selection are payback period (PB), internal rate of return (IRR), and net present value (NPV).

How is net present value used in capital budgeting?

The net present value approach is the most intuitive and accurate valuation approach to capital budgeting problems. Discounting the after-tax cash flows by the weighted average cost of capital allows managers to determine whether a project will be profitable or not.

Why do you need a capital budget spreadsheet?

In other cases, a separate estimation or assumption of the Project Cost of Capital is required. This Capital Budgeting spreadsheet aims to assist investors, managers or analysts in correctly estimating the cash flow in different scenarios and accurately calculating the Net Present Value and Internal Rate of Return.

How is the PB used to determine capital budgeting decisions?

There are drawbacks to using the PB metric to determine capital budgeting decisions. Firstly, the payback period does not account for the time value of money (TVM). Simply calculating the PB provides a metric which places the same emphasis on payments received in year one and year two.