To compute the value of the flexible budget, multiply the variable cost per unit by the actual production volume. Here, the figure indicates that the variable costs of producing 125,000 should total $162,500 (125,000 units x $1.30).

What is meant by flexible budget?

A flexible budget is a budget that adjusts to the activity or volume levels of a company. Unlike a static budget, which does not change from the amounts established when the budget was created, a flexible budget continuously “flexes” with a business’s variations in costs.

Why a flexible budget can improve performance evaluations?

The flexible budget responds to changes in activity, and may provide a better tool for performance evaluation. It is driven by the expected cost behavior. Fixed factory overhead is the same no matter the activity level, and variable costs are a direct function of observed activity.

How are flexible budget variances determined?

A flexible budget variance is any difference between the results generated by a flexible budget model and actual results. If actual revenues are inserted into a flexible budget model, this means that any variance will arise between budgeted and actual expenses, not revenues.

What is flexible budget based on?

A flexible budget adjusts based on changes in actual revenue or other activities. The result is a budget that is fairly closely aligned with actual results. This approach varies from the more common static budget, which contains nothing but fixed expense amounts that do not vary with actual revenue levels.

How to create a flexible budget with example?

Divide the budget you plan on spending on variable costs by your estimated production. This will provide a starting budget for cost per unit. 3. Create your budget with set fixed costs Create your budget with set fixed costs that will not change and variable costs depicted as percentages that can be adjusted based on actual revenue.

How are fixed costs adjusted in a flexible budget?

Key Concepts and Summary 1 The fixed manufacturing overhead is adjusted for units sold in the flexible budget. 2 The variable manufacturing overhead is adjusted in the static budget. 3 There is no difference between the budgets. 4 The variable costs are adjusted in a flexible budget.

How to calculate flexible budget for 70% capacity?

The table below shows the calculations for units produced at 70% capacity and calculates the variable cost per unit for all variable costs. Now that we know the variable costs per unit. we can calculate the flexible budget for any level of activity using these figures. Leed Company prepares a flexible budget for 70%, 80%, 90% and 100% capacity.

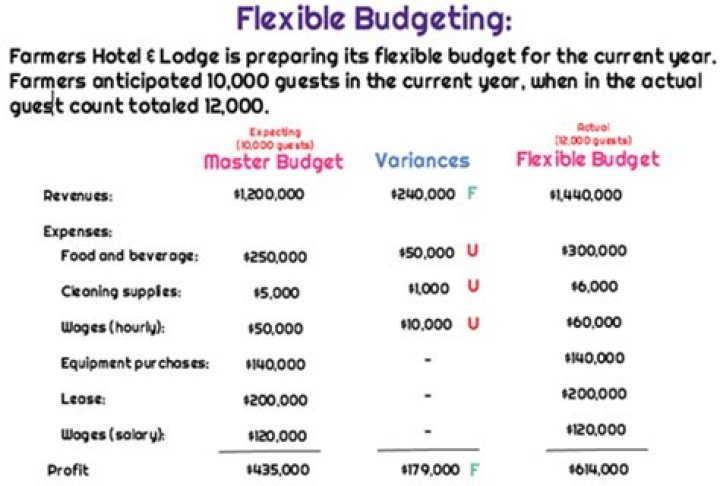

What is the difference between a Master Budget and a flexible budget?

To understand differences in spending, or costs, these flexible budget formulas are used: Per-unit variable cost – the cost to produce a single unit. Per-unit revenue – the amount charged per unit. Total fixed cost – a fixed amount added to the budget regardless of the number of units produced or sales activity. A master budget is rarely perfect.