In terms of computing the amount:

- Contribution Margin = Net Sales Revenue – Variable Costs.

- Contribution Margin = Fixed Costs + Net Income.

- Contribution Margin Ratio = (Net Sales Revenue -Variable Costs ) / (Sales Revenue)

Is contribution the same as fixed costs?

Contribution isn’t directly related to fixed costs, though it does have a correlation in the progression toward net profit or loss.

What is a company’s total fixed costs?

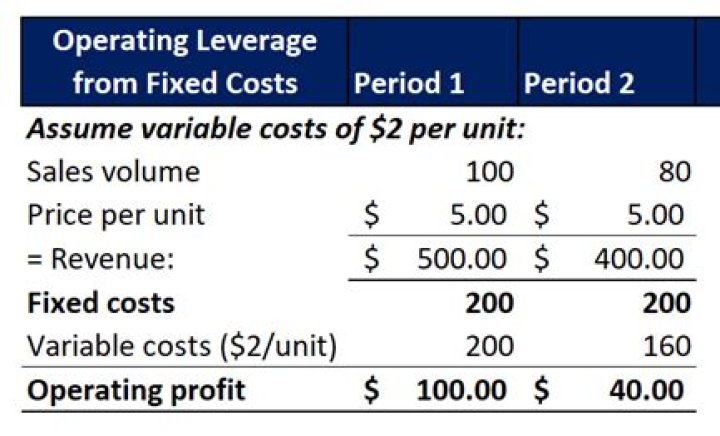

Total fixed costs are the sum of all consistent, non-variable expenses a company must pay. For example, suppose a company leases office space for $10,000 per month, rents machinery for $5,000 per month, and has a $1,000 monthly utility bill. In this case, the company’s total fixed costs would be $16,000.

What are high fixed costs?

Fixed costs are usually negotiated for a specified time period and do not change with production levels. Examples of fixed costs include rental lease payments, salaries, insurance, property taxes, interest expenses, depreciation, and potentially some utilities.

What companies have high fixed costs?

They require only office spaces, office supplies, etc. Other high fixed cost companies are airlines, automobile manufacturers, and pharmaceutical companies. Any of these industries require large amounts of capital investments or R&D expenditures (research and development expenses).

Formula for Contribution Margin

- Contribution Margin = Net Sales Revenue – Variable Costs.

- Contribution Margin = Fixed Costs + Net Income.

- Contribution Margin Ratio = (Net Sales Revenue -Variable Costs ) / (Sales Revenue)

How do you calculate business a level contributions?

- Definition:

- Total Contribution is the difference between Total Sales and Total Variable Costs.

- Formulae:

- Contribution = total sales less total variable costs.

- Contribution per unit = selling price per unit less variable costs per unit.

- Contribution per unit x number of units sold.

How do you calculate contribution ratio?

Contribution margin ratio = contribution margin / sales (where contribution margin = sales minus variable costs). The contribution margin ratio can help companies calculate and set targets for the profit potential of a given product.