Covariance is calculated by analyzing at-return surprises (standard deviations from the expected return) or by multiplying the correlation between the two variables by the standard deviation of each variable.

Does covariance affect expected return?

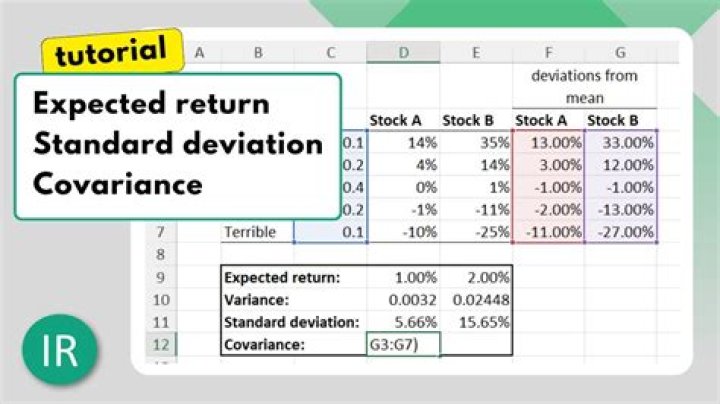

A positive covariance indicates that two assets move in tandem. A negative covariance indicates that two assets move in opposite directions. In the construction of a portfolio, it is important to attempt to reduce the overall risk and volatility while striving for a positive rate of return.

How do you calculate expected return and risk?

The expected return is the amount of profit or loss an investor can anticipate receiving on an investment. An expected return is calculated by multiplying potential outcomes by the odds of them occurring and then totaling these results.

How do you calculate expected market return?

Expected return = Risk Free Rate + [Beta x Market Return Premium]

Is positive covariance good?

A positive covariance means asset prices are moving in the same general direction. A negative covariance means asset prices are moving in opposite directions. Covariance helps investors create a portfolio that includes a mix of distinct asset types, thus employing a diversification strategy to reduce risk.

How do you calculate at risk?

What does it mean? Many authors refer to risk as the probability of loss multiplied by the amount of loss (in monetary terms).

What is the current market rate of return?

While that sounds like a good overall return, not every year has been the same. While the S&P 500 fell more than 4% between the first and last day of 2018, values and dividends increased by 31.5% during 2019….

| Year | S&P 500 annual return |

|---|---|

| 2017 | 21.8% |

| 2018 | -4.4% |

| 2019 | 31.5% |

| 2020 | 18.4% |

What is the difference between covariance and correlation?

Correlation refers to the scaled form of covariance. Covariance indicates the direction of the linear relationship between variables. Correlation on the other hand measures both the strength and direction of the linear relationship between two variables. Covariance is affected by the change in scale.

Should I use correlation or covariance?

Correlation matrix or the covariance matrix? In simple words, you are advised to use the covariance matrix when the variable are on similar scales and the correlation matrix when the scales of the variables differ.

Where is correlation and covariance used?

Covariance is a measure to indicate the extent to which two random variables change in tandem. Correlation is a measure used to represent how strongly two random variables are related to each other. Covariance is nothing but a measure of correlation. Correlation refers to the scaled form of covariance.

What is var formula?

Value at Risk (VAR) calculates the maximum loss expected (or worst case scenario) on an investment, over a given time period and given a specified degree of confidence. We looked at three methods commonly used to calculate VAR.

How do you calculate a day VAR?

Value at Risk (VAR) can also be stated as a percentage of the portfolio i.e. a specific percentage of the portfolio is the VAR of the portfolio. For example, if its 5% VAR of 2% over the next 1 day and the portfolio value is $10,000, then it is equivalent to 5% VAR of $200 (2% of $10,000) over the next 1 day.