In MACRS straight line, LN calculates the percentage for a year by dividing one depreciation period by the remaining life of the asset, and then applying this amount with the averaging convention to determine the depreciation amount for that year.

When did MACRS depreciation start?

1986

The MACRS method was introduced in 1986, and generally property placed into service after that date will be depreciated according to the MACRS method. It is a modification of the Accelerated Cost Recovery System, or ACRS, which was in use from 1981 to 1986.

Do you take depreciation in the year of sale?

Data source: IRS. In the year you sell a rental property, this works the opposite way. You can take the depreciation deduction for the months the property was in service (prior to the sale). Another case where you might take a partial depreciation deduction is in the year when your deduction has been used up.

What is the MACRS depreciation schedule?

The modified accelerated cost recovery system (MACRS) is a depreciation system used for tax purposes in the U.S. MACRS depreciation allows the capitalized cost of an asset to be recovered over a specified period via annual deductions. The MACRS system puts fixed assets into classes that have set depreciation periods.

Is MACRS depreciation the same every year?

The MACRS depreciation method allows for larger deductions in the early years of an asset’s life, and lower deductions in later years. This contrasts significantly with straight-line depreciation, wherein you claim the same tax deduction each year, until the end of the asset’s usable life.

Can you elect out of MACRS depreciation?

Generally, if you exercise your option to use any of the variations of MACRS you must use it for all assets of the same class that you placed in service during the year. Once you make the election you cannot change it.

What is the special depreciation allowance for 2020?

30%

Certain qualified property with a long production period and certain aircraft acquired before September 28, 2017, and placed in service in 2020, is eligible for a 30% special depreciation allowance. Qualified property must also be placed in service before January 1, 2021.

Is MACRS double declining?

Under MACRS, a company must use different depreciation methods for different classes of assets. For heavy machinery, MACRS requires that companies set the taxable life at 10 years and use a “double-declining” method. This method depreciates the asset by 20 percent of its value at the beginning of each tax year.

Is Macrs depreciation mandatory?

MACRS required for most property. For most business property placed in service after 1986, you must depreciate the asset using a method called the Modified Accelerated Cost Recovery Method (MACRS).

Do you subtract depreciation from taxable income?

A company’s depreciation expense reduces the amount of earnings on which taxes are based, thus reducing the amount of taxes owed. The larger the depreciation expense, the lower the taxable income, and the lower a company’s tax bill.

Is MACRS depreciation required for tax purposes?

The modified accelerated cost recovery system (MACRS) is the proper depreciation method for most assets. For property placed into service after 1986, the IRS requires businesses use MACRS for depreciation.

How is deferred tax liability calculated?

The deferred tax liability represents a future tax payment a company is expected to make to appropriate tax authorities in the future, and it is calculated as the company’s anticipated tax rate times the difference between its taxable income and accounting earnings before taxes.

Is depreciation a tax credit or deduction?

Depreciation is a tax deduction that allows you to recover the cost of assets that you purchase and use for your business. Once you’ve calculated depreciation, you must complete Form 4562 to claim your tax deduction for each asset.

How many months can you depreciate a home under MACRS?

This means that your tax deduction is limited to 6 months in the year that you placed the property in service and the year that it is disposed of. There are 4 MACRS depreciation methods. Three of them fall under the GDS system, and the fourth method falls under the ADS system.

How does the half year convention affect depreciation?

The half-year convention treats all property as if it were placed in service or disposed of at the midpoint of the year. This means that your tax deduction is limited to 6 months in the year that you placed the property in service and the year that it is disposed of.

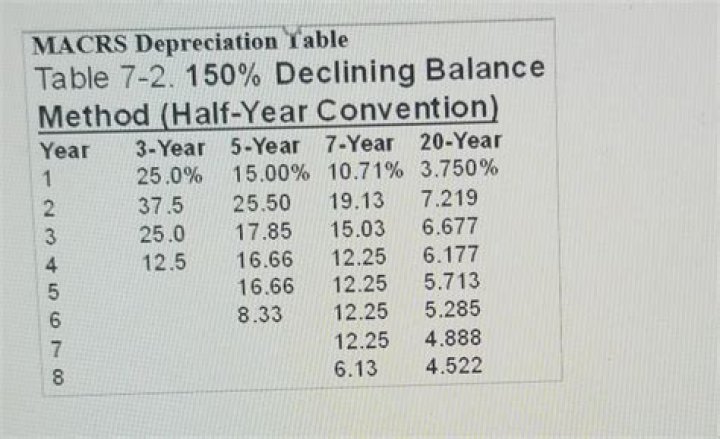

Which is MACRS table do you use to calculate depreciation?

Using the MACRS Percentage Table Guide (above), you can determine which depreciation rate table (below) you will need to use. There are about 18 depreciation rate tables provided by the IRS. Below is a snapshot of just two of the tables. You can find a full list of the tables in IRS Pub 946, Appendix A.

How many depreciation tables are there on the IRS website?

There are about 18 depreciation rate tables provided by the IRS. Below is a snapshot of just two of the tables. You can find a full list of the tables in IRS Pub 946, Appendix A. From this table you can get the depreciation rate allowed for each year of the asset’s useful life or recovery period.