Straight-Line Method

- Subtract the asset’s salvage value from its cost to determine the amount that can be depreciated.

- Divide this amount by the number of years in the asset’s useful lifespan.

- Divide by 12 to tell you the monthly depreciation for the asset.

When an asset is bought in the previous year and put to use for 180 days or less how much is the depreciation to be allowed?

The rate of additional depreciation is 20% of the actual cost if asset is acquired and put to use for 180 days or more. The rate shall be 10% if period is less than 180 days, but a sum of 10% is allowed in the immediate next previous year.

Do assets depreciate in the first year?

After the first year, the asset will depreciate in the same manner as Full Month. Half Year: One half of a normal year’s depreciation will be depreciated in the first year. The actual amount of depreciation will be distributed over the number of periods the asset is in service during the first year.

Do assets depreciate if not in use?

Therefore, depreciation does not cease when the asset becomes idle or is retired from active use unless the asset is fully depreciated. However, under usage methods of depreciation the depreciation charge can be zero while there is no production.

Is depreciation allowed in the year of sale of asset?

Depreciation is allowable as expense in Income Tax Act, 1961 on basis of block of assets on Written Down Value (WDV) method. Depreciation on Straight Line Method (SLM) is not allowed. Block of assets means group of assets falling within a class of assets for which same rate of depreciation is prescribed.

How much can I depreciate an asset?

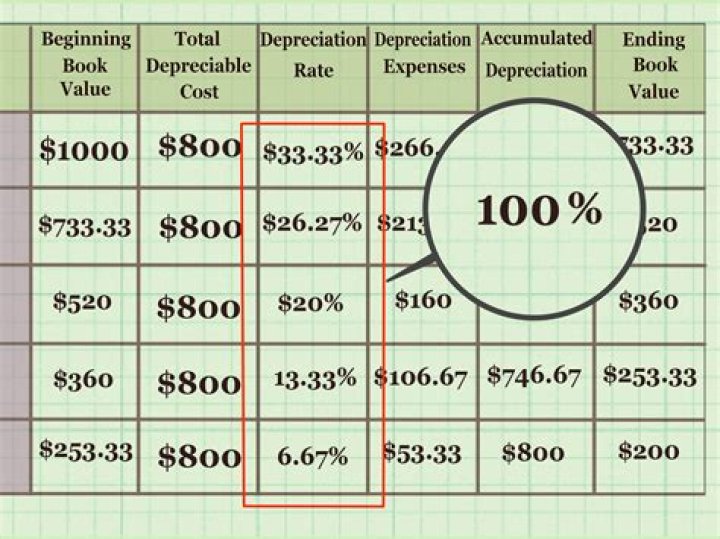

There are two estimates needed: 1) the number of years that the asset will be used, and 2) the salvage value at the end of the asset’s use. If an asset has a cost of $100,000 and is expected to be used for 10 years and then have no salvage value, most companies will depreciate the asset at the rate of $10,000 per year.

What happens when an asset is not used?

If asset is not used then depreciation will not be charged on it during the year. Depreciation is calculated from the time The Asset is Put into use (or placed into service). The asset’s cost should be matched with the revenues earned by using the asset, i.e. depreciation must be spread out over the periods in which revenue is earned.

What happens if an asset is sold on a day other than December 31?

Similarly, if an asset is sold on a day other than December 31, less than a full year’s depreciation is assigned to the year of sale. Once again, revenue is not generated for the entire period; depreciation expense must also be recognized proportionally.

Can you depreciate an asset if it is not used?

…and used for the purposes of the business21 or profession… in this regard, if asset not used during the year, no depreciation to be allowed. 27 June 2010 It says date of put to use.. As you mentioned that it is not used than no depreciation…

When is depreciation allowed on whole block of assets?

Depreciation is allowed on whole block of asset even if only a single asset in that block is used during the year at any point of time. WDV of an asset = Actual cost to the assesse – All depreciation actually allowed to him (included unabsorbed depreciation, if any) WDV at the end of the year XXX