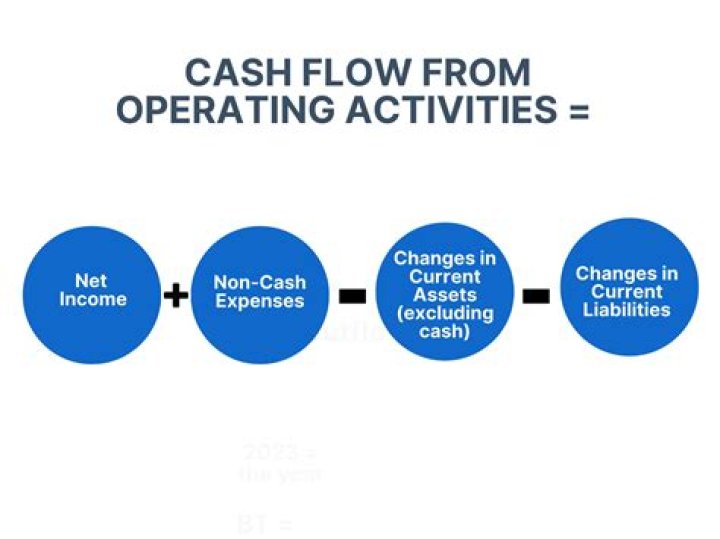

Calculating Cash Flow from Operations using Indirect Method

- Start with Net Income.

- Subtract: Identify gains or losses that result from financing and investments (like gains from the sale of land)

- Add: Non-cash charges to income (such as depreciation and goodwill amortization.

- Add or subtract changes to operating accounts.

What is the difference between direct and indirect cash?

The cash flow direct method determines changes in cash receipts and payments, which are reported in the cash flow from the operations section. The indirect method takes the net income generated in a period and adds or subtracts changes in the asset and liability accounts to determine the implied cash flow.

With the indirect method, cash flow is calculated by taking the value of the net income (i.e. net profit) at the end of the reporting period. You then adjust this net income value based on figures within the balance sheet and strip-out the effect of non-cash movements shown on the profit and loss statement.

What are the two methods used in cash flow preparation for operating activities?

There are two methods for depicting cash from operating activities on a cash flow statement: the indirect method and the direct method. The indirect method begins with net income from the income statement then adds back noncash items to arrive at a cash basis figure.

What is an example of cash flow from operating activities?

Examples of cash inflows from operating activities are: Cash receipts from the sale of goods and services. Cash receipts from the collection of receivables. Cash receipts from lawsuit settlements.

How is net cash flow from operating activities calculated?

Here we will study the indirect method to calculate cash flows from operating activities. In indirect method, the net income figure from the income statement is used to calculate the amount of net cash flow from operating activities.

How to calculate cash flow from operations for ABC Corporation?

ABC Corporation’s income statement sales was $650,000; gross profit of $350,000; selling and administrative costs of $140,000; and income taxes of $40,000. The selling and administrative expenses included $14,500 for depreciation. Calculate Cash Flow from Operations using the Direct Method.

Where does net income go in a cash flow statement?

This typically includes net income from the income statement, adjustments to net income, and changes in working capital. Net income is typically the first line item in the operating activities section of the cash flow statement.

Which is the direct method of operating activities?

Direct method of operating activities cash flows is one of the two main techniques that may be used to calculate the net cash flow from operating activities in a cash flow statement, the other being indirect method.