Review existing procedures (if any) laid down by the management to identify these events. Study minutes of the meetings of the Members, Board of the directors and other important executive committees (if any) held after the balance sheet date and enquire about the matters which may be relevant in this regard.

What is the auditors role in testing subsequent events?

10, the auditor identifies subsequent events that require adjustment of, or disclosure in, the financial statements, the auditor should determine whether each such event is appropriately reflected in the financial statements in accor- dance with the applicable financial reporting framework.

What subsequent events require disclosure?

Subsequent Events: When Do I Record and When Do I Disclose?

- Sale of a bond or capital stock issued after the balance sheet date;

- A business combination that occurs after the balance sheet date;

- Settlement of litigation when the event giving rise to the claim took place after the balance sheet date;

What is commonly referred to in auditing as a subsequent event?

a) The subsequent events refer to an event occurring after the balance sheet date, but before the date of issuance of the auditor’s report. The subsequent event might have a material effect on the company’s financial statements. Therefore, it might require a disclosure and some adjustment to the financial statements.

What is a recognized subsequent event?

Recognized or type 1 subsequent events are typically events that occurred at the financial statement date. But that may have concluded after the year end. The financial statements must then be altered to include this event because it would be misleading not to list the event.

What is a Type 2 subsequent event?

Type II subsequent events provide evidence about conditions that did not exist on or before the balance sheet date. These events are disclosed, but are not recognized in the financial statements.

What are subsequent auditors?

In case of subsequent auditor for existing government companies, the Comptroller & Auditor General shall appoint the auditor within a period of 180 days from the commencement of the financial year and the auditor so appointed shall hold his position till the conclusion of the Annual General Meeting.

What is definition of subsequent event what the different between Type 1 and Type 2 subsequent event?

Type I subsequent events provide evidence about conditions that existed on or before the balance sheet date. Type II subsequent events provide evidence about conditions that did not exist on or before the balance sheet date. These events are disclosed, but are not recognized in the financial statements.

What are the two types of subsequent events in auditing?

There are two types of subsequent events:

- Adjusting events. An event that provides additional information about pre-existing conditions that existed on the balance sheet date.

- Non-adjusting events. A subsequent event that provides new information about a condition that did not exist on the balance sheet date.

What are the types of subsequent events?

What would be an adjusting subsequent event?

Adjusting events An event that provides additional information about pre-existing conditions that existed on the balance sheet date.

What is the difference between Type 1 and Type 2 subsequent events?

Subsequent events fall into one of two categories, each with its own accounting rules: Type I subsequent events provide evidence about conditions that existed on or before the balance sheet date. Type II subsequent events provide evidence about conditions that did not exist on or before the balance sheet date.

How are subsequent auditors appointed?

The Subsequent Auditor shall be appointed at the 1st AGM by the shareholders of the company by passing O/R and such Auditor shall hold office for next 5 years.

What is a Type II subsequent event?

The second type consists of those events that provide evidence with respect to conditions that did not exist at the date of the balance sheet being reported on but arose subsequent to that date. These events should not result in adjustment of the financial statements. fn1.

Can auditor be appointed for 5 years in EGM?

(EGM shall be conducted within 3 months from the date of recommendation of the Board). 4. Otherwise, such auditor can be re-appointed for a period of 5 years under section 139(1) of Companies Act, 2013. Company is required to file Form ADT-1 within 15 days from the date of appointment in a general meeting.

Can auditor be appointed for 2 years?

Thus, one can opine that the auditor cannot be appointed for one term, consisting of period less than or more than five years. If any new auditor (other than first Auditor) is appointed in the first AGM, no need to file e- form ADT-3 as the term of the first Auditor is only till the conclusion of first AGM.

Can we appoint first auditor for 5 years?

Individuals as an Auditor cannot be appointed as an Auditor for a term of more than 5 years. A firm of Auditors cannot be appointed as Auditors for more than two terms of 5 years.

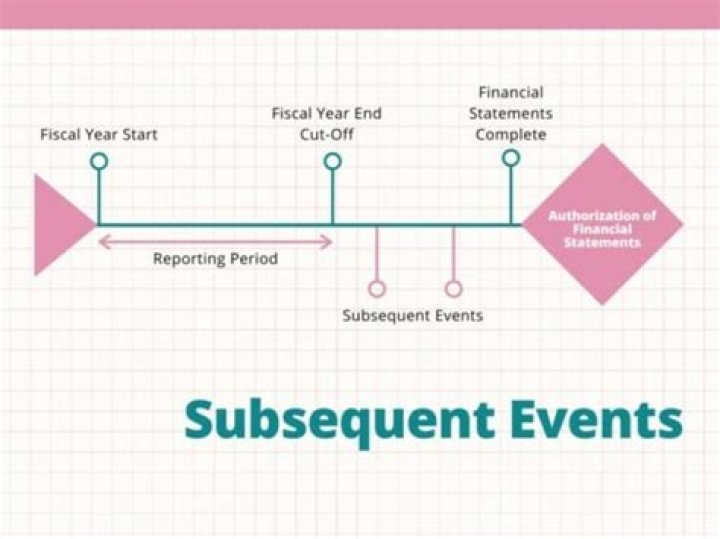

What are subsequent events in the reporting audit stage?

In this ISA, the term “subsequent events” is used to refer to both events occurring between the date of the financial statements and the date of the auditor’s report, and facts discovered after the date of the auditor’s report.

There are generally two types of subsequent events. 1)The first is a recognized event whereas the second is a non-recognized event. Recognized or type 1 subsequent events are typically events that occurred at the financial statement date. But that may have concluded after the year end.

Which would be an adjusting subsequent event?

If events take place before the balance sheet date that trigger a lawsuit, and lawsuit settlement is a subsequent event, consider adjusting the amount of any contingent loss already recognized to match the amount of the actual settlement.

When do you need to include subsequent events in an audit?

List the audit procedures that may be performed by the auditor in order to ensure that all events occurring between the date of the financial statements and the date of the auditor’s report that require adjustment of, or disclosure in, the financial statements are identified and appropriately reflected in the financial statements.

What are the procedures for identifying subsequent events?

Audit Procedures in identifying Subsequent Events that require either adjustment or disclosure in the financial statements.

What are Type II subsequent events in accounting?

Type II subsequent events provide evidence about conditions that did not exist on or before the balance sheet date. These events are disclosed, but are not recognized in the financial statements. These events are disclosed, but are not recognized in the financial statements.

When to record and when to disclose subsequent events?

That date is either the date the financial statements were issued or the date the financial statements were available to be issued. Additionally, certain unrecognized subsequent events must be disclosed if they are in such nature that omitting them would cause the financial statements to be misleading.