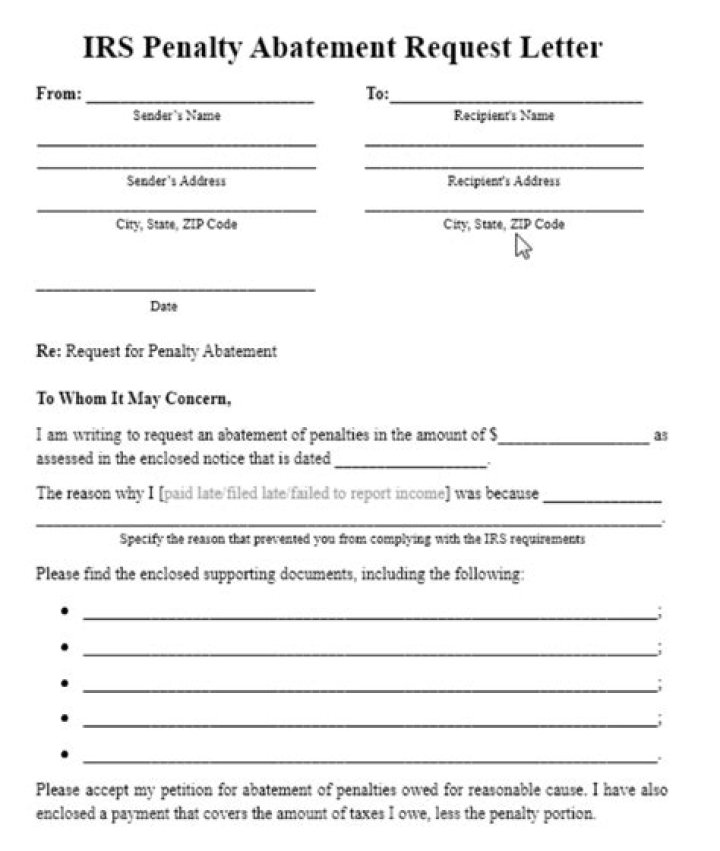

Methods for Requesting Penalty Relief After the IRS has assessed a penalty, the taxpayer can request penalty abatement, typically by writing a penalty abatement letter or by calling the IRS. Tax professionals can also request abatement using IRS e-services.

What is considered reasonable cause for penalty abatement?

Reasonable Cause is based on all the facts and circumstances in your situation. We will consider any reason which establishes that you used all ordinary business care and prudence to meet your Federal tax obligations but were nevertheless unable to do so.

Can estimated tax penalty be abated?

ESTIMATED TAX PENALTY (SEC. The IRS may abate it if the taxpayer (1) proves that the IRS incorrectly charged the penalty or made an error, (2) shows that calculating the penalty under a different method reduces or eliminates it, or (3) proves that he or she meets the waiver criteria discussed in Sec.

What do you need to know about IRS penalty abatement?

A qualified tax professional will provide you with the information you need to be successful in your IRS penalty abatement. If you want an understanding of what the IRS is looking for, you may send a sample penalty abatement letter.

When to seek abatement of New York state tax?

This entry was posted in New York State Income Tax, NYS Penalties, Penalties and tagged 20 NYCRR § 2392, abatement, reasonable cause, tax penalties, willful neglect. Bookmark the permalink .

Can a trust fund be used for tax abatement?

Form 843 may also be used for trust fund recovery penalty abatements as well. While you can apply for an abatement without the help of a tax professional abatement services, it’s not suggested.

When to seek waiver of penalties and interest?

20 NYCRR § 536.1(c), entitled “Penalties and interest,” provides for waiver of penalties if a taxpayer’s failure to pay “was due to reasonable cause and not due to willful neglect.