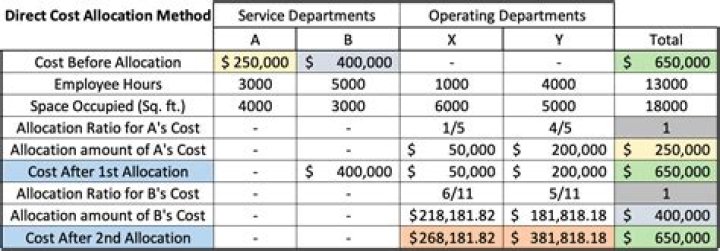

The first method, the direct method, is the simplest of the three. The direct method allocates costs of each of the service departments to each operating department based on each department’s share of the allocation base. Services used by other service departments are ignored.

How do you allocate cost to department?

There are three methods for allocating service department costs: direct, sequential, and reciprocal. The first step of each method is to classify each organizational unit as either an operating or service department.

What are the three primary methods of cost allocation?

There are three methods commonly used to allocate support costs: (1) the direct method; (2) the sequential (or step) method; and (3) the reciprocal method.

Which cost allocation method is the best?

There are three primary cost allocation methods used by organizations based on how the expenditures are generated. The step method is best when all costs are internal. For this method, one department within an organization provides a service directly to another.

Why do we use allocation methods?

Various cost allocation methods are used to allocate factory overhead costs to units of production. Allocations are performed in order to create financial statements that are in compliance with the applicable accounting framework. Overhead is applied based on the amount of direct labor consumed by a unit of production.

How is the high low method used?

The high-low method is used to calculate the variable and fixed cost of a product or entity with mixed costs. It considers the total dollars of the mixed costs at the highest volume of activity and the total dollars of the mixed costs at the lowest volume of activity.

How do you allocate direct method?

Direct allocation method. Charge the applicable cost of these departments directly to the production part of the business. These costs form a portion of the overhead cost of production, which is then allocated to inventory and the cost of goods sold.

How are service department costs allocated?

WHAT IS department allocation?

An allocation base is the basis upon which an entity allocates its overhead costs. The typical allocation process in a multi-department company is: Allocate service department costs to operating departments. Assign operating department costs (including the allocations from service departments) to products and services.

How costs are allocated?

Cost allocation is the process of identifying, accumulating, and assigning costs to costs objects such as departments, products, programs, or a branch of a company. If costs are allocated to the wrong cost objects, the company may be assigning resources to cost objects that do not yield as much profits as expected.

What are cost allocation methods?

Cost allocation methods take a shared service, such as company-wide technical support, by allowing an organization to properly assign associated expenses to each department based on how they use the service, clarifying and validating expenditures.

How does the direct method of allocation work?

The direct method allocates costs of each of the service departments to each operating department based on each department’s share of the allocation base. Services used by other service departments are ignored.

How to calculate the service department allocation rate?

We can calculate the service department allocation rates as follows: To allocate the service department costs to each operating department, we will take the amount of the cost driver (machine hours for maintenance and employees for administration) x the allocation rate we just calculated.

Which is an example of the direct method?

Services used by other service departments are ignored. This means the direct method does not recognize service performed by other service departments. For example, if Service Department A uses some of Service Department B’s services, these services would be ignored in the cost allocation process.

What are the advantages and disadvantages of direct cost allocation?

Advantages and disadvantages of direct method of cost allocation. Many organizations use direct method for allocating departmental costs because it is very simple and easy to employ. The major disadvantage of direct method is that it ignores interdepartmental services and can therefore lead to distorted products and services cost.