A life settlement refers to the sale of an existing insurance policy to a third party for a one-time cash payment. After the sale, the purchaser becomes the policy’s beneficiary and assumes payment of its premiums. By doing so, they receive the death benefit when the insured dies.

Are life settlements Legal?

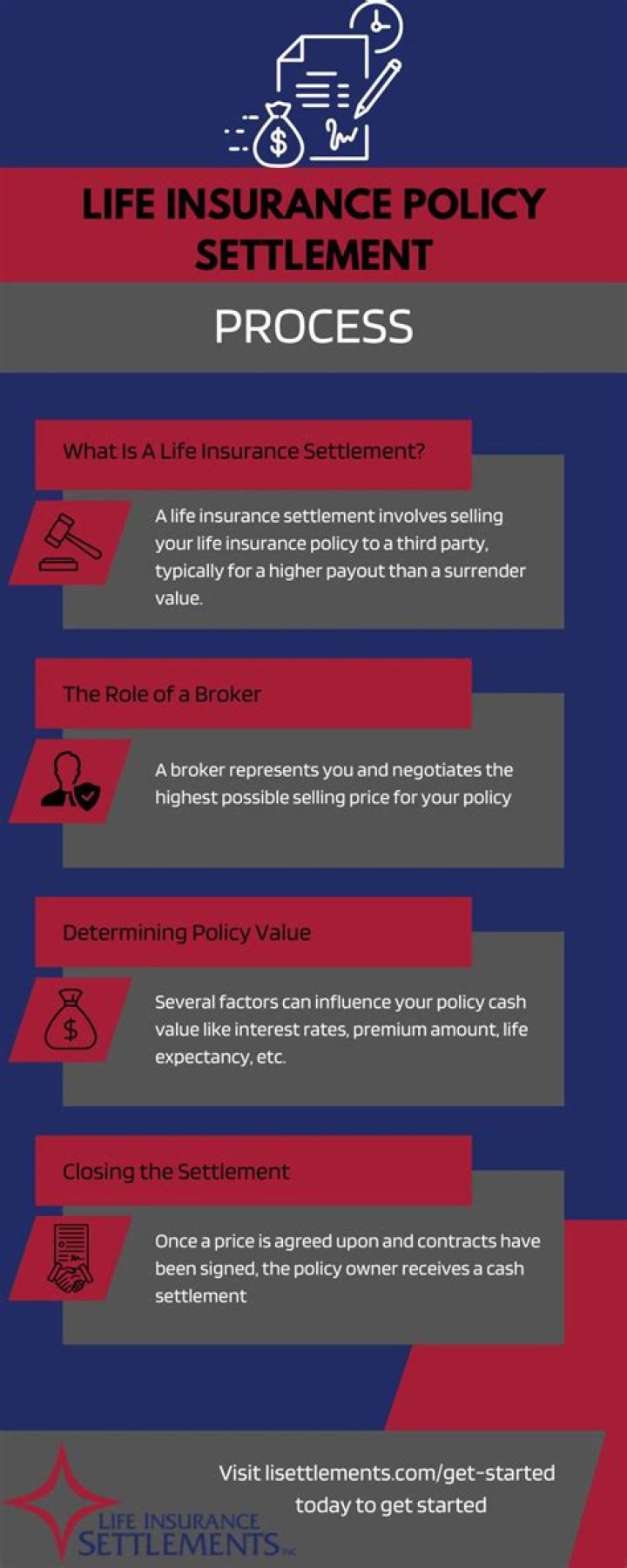

A life settlement is the legal sale of an existing life insurance policy (typically of seniors) for more than its cash surrender value, but less than its net death benefit, to a third party investor.

Who is the owner in a life settlement contract?

VIATICAL SETTLEMENT PURCHASER A person who invests in one or more viatical contracts. Policyowner – The person or party who owns an insurance policy. The policyowner is usually the insured and/or the beneficiary, but can be someone else. The policyowner is the only person who can make changes to a policy.

What do you need to know about life settlements?

Life settlements are commercial transactions where life insurance policy holders (usually individuals) sell their life insurance policy to a third party. 4 National Council of Insurance Legislators (NCOIL) Life Settlements Model Act, §2(B). 5 Id. 6 Health Insurance Portability and Accountability Act (HIPAA), P.L. 104-191.

Who is on the buy side of life settlement?

In the life settlement industry, there is a buy – side and a sell – side similar to other investments. It is important to understand who sits on the same side of the table with the CPA and the client in the life settlement process. On the buy – side, a life settlement provider/buyeris the representative for the institutional investors.

Why did Amy buy a life insurance policy?

4) Amy purchased a life insurance policy with the intent of committing suicide to pay all the debts that were burdening her family. If she commits suicide 9 months after the policy is purchased, and the insurer is able to prove that her death was a suicide, how much will be paid by the insurance company?

How old was Lionel when he bought life insurance?

44) Lionel purchased a $200,000 ordinary life insurance policy when he was 25 years old and had significant life insurance needs. Now Lionel is 50. His mortgage is almost paid-off and his children have left home and are financially independent. Lionel no longer wants to pay premiums, but he would like to have some permanent life insurance in force.