It may be helpful to talk to a tax professional about the implications of taking a non-qualified distribution from a Roth IRA. If you take an early distribution that’s subject to taxes and penalties, they can also help you file Form 5329 to report those distributions.

Do you have to report Roth IRA distributions on taxes?

Tax Reporting for Qualified Distributions Even though qualified Roth IRA distributions aren’t taxable, you must still report them on your tax return using either Form 1040 or Form 1040A. If you opt to use Form 1040 to file your taxes, enter the nontaxable amount of your qualified distribution on line 15a.

What are non-qualified distributions from Roth IRA?

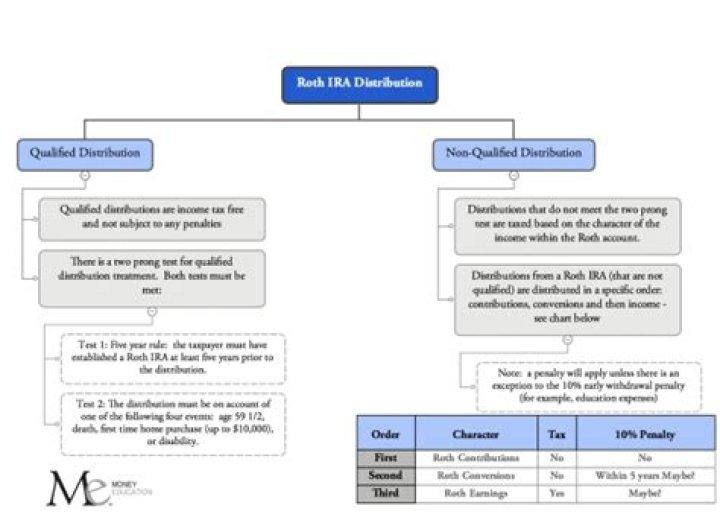

A non-qualified distribution can refer to two scenarios: either a distribution from a Roth IRA that occurs before the IRA owner meets certain requirements or a distribution from an education savings account that exceeds the amount used for qualified education expenses.

Are distributions from a Roth IRA considered income?

Earnings from a Roth IRA don’t count as income as long as withdrawals are considered qualified. If you take a non-qualified distribution, it counts as taxable income, and you might also have to pay a penalty.

Do you get a 1099 for a Roth IRA distribution?

Retirement accounts, including Traditional, Roth and SEP IRAs, will receive a Form 1099-R only if a distribution (withdrawal) was made during the year. If you made no contributions to your IRA for the year and took no distributions, you will not receive tax documents for your retirement account.

Are Roth distributions considered income?

The easy answer is that earnings from a Roth IRA do not count towards income. If you keep the earnings within the account, they definitely are not taxable. Generally, they still do not count as income—unless the withdrawal is considered a non-qualified distribution.

When to take a non qualified distribution from a Roth IRA?

A non-qualified distribution from an Roth IRA is any distribution that doesn’t follow the guidelines for Roth IRA qualified distributions. Specifically, that means distribution: Taken before age 59.5.

Do you have to report Roth IRA distributions?

However, even if you meet the requirements for a qualified Roth IRA distribution, the Internal Revenue Service still requires that you report your Roth IRA distributions on your income tax return.

What are the tax implications of a non qualified distribution?

The tax implications of a non-qualified distribution depend on the source of the Roth IRA assets. There are four possible sources of Roth IRA assets: Regular participant contributions and rollover of basis from designated Roth accounts.

What are the tax consequences of a Roth IRA distribution?

First of all, distributions of Roth IRA assets from regular participant contributions and from nontaxable conversions can be taken at any time, tax- and penalty-free. However, distributions on taxable conversion amounts may be subject to the 10% early distribution penalty.