Under the general rule, the trust serves as an information reporter. The trust must obtain its own taxpayer identification number (TIN). However, income is not reported on the trust’s Form 1041. Income is reported on an attachment to the Form 1041, which also identifies the grantor as the owner of trust income.

Do grantor trusts issue 1099s?

The trustee turns around and issues 1099s to the grantor. So, you might have 10, 11, 12 1099s coming in or K-1s coming in and then you turn around and you issue 1099s to the grantor. Then you ship all of these things off on a Form 1096, which is the transmittal form that you send to the IRS.

What tax form does a grantor trust file?

Form 1041

The general rule is that all grantor trusts must file a Form 1041, which contains only the trust’s name, address, and tax identification number (TIN) (see Regs.

Does an irrevocable grantor trust have to file a tax return?

If an irrevocable trust has its own tax ID number, then the IRS requires the trust to file its own income tax return, which is IRS form 1041. During the lifetime of the grantor, any interest, dividends, or realized gains on the assets of the trust are taxable on the grantor’s 1040 individual income tax return.

What happens when the grantor of an irrevocable trust dies?

When the grantor, who is also the trustee, dies, the successor trustee named in the Declaration of Trust takes over as trustee. The new trustee is responsible for distributing the trust property to the beneficiaries named in the trust document. That person may or may not be the successor trustee.

Can a grantor trust make distributions?

A grantor trust, such as revocable trust, is taxed directly to the grantor and the grantor reports the income of the trust on his or her own Form 1040. If the trust makes distributions during the tax year to beneficiaries, those distributions may carry out taxable income of the trust.

Can a grantor take money from an irrevocable trust?

Irrevocable Trust Basics An irrevocable trust has a grantor, a trustee, and a beneficiary or beneficiaries. Once the grantor places an asset in an irrevocable trust, it is a gift to the trust and the grantor cannot revoke it. To take advantage of the estate tax exemption and remove taxable assets from the estate.

What happens to an irrevocable grantor trust when the grantor dies?

Death of the Grantor of a Trust When the grantor of an individual living trust dies, the trust becomes irrevocable. This means no changes can be made to the trust. If the grantor was also the trustee, it is at this point that the successor trustee steps in. There is one exception to this rule.

Do you have to file a grantor trust return?

Revocable trusts (Grantor Trusts) are not required to file a tax return or form 1041. When grantor trust status applies, either the grantor or a beneficiary is treated as the owner of the activity inside the trust for income tax purposes.

Who pays taxes on a grantor trust?

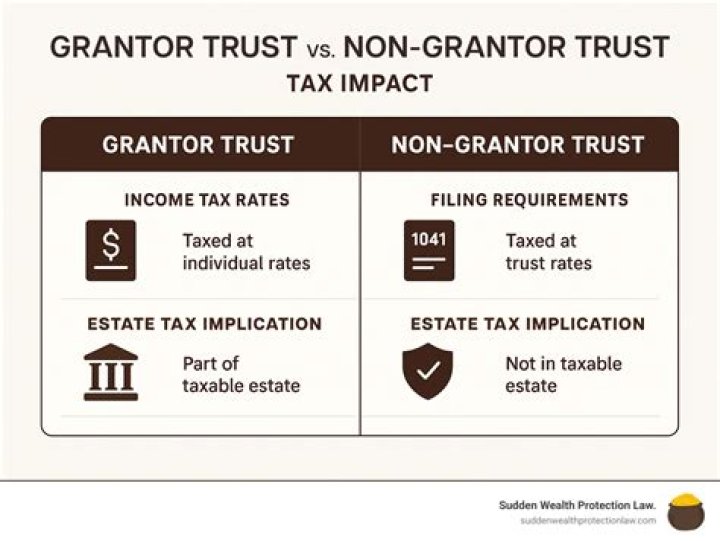

If a trust is a grantor trust, then the grantor is treated as the owner of the assets, the trust is disregarded as a separate tax entity, and all income is taxed to the grantor.

Who pays the taxes on an irrevocable grantor trust?

For taxation purposes, trusts can typically be divided into two camps: Grantor trusts: All income is taxed to the grantor, regardless of whether the grantor receives distributions from the trust. These trusts are treated as “alter egos” of the grantor for income tax purposes.

Does a trust become irrevocable when the grantor dies?

A revocable trust is a method of protecting assets from probate should the grantor of the trust die. An irrevocable trust is one that cannot be modified by the grantor. Upon the death of the grantor, a revocable trust automatically becomes irrevocable.

How are distributions from a grantor trust taxed?

Does a grantor trust end when the grantor dies?

Upon the death of the grantor, grantor trust status terminates, and all pre-death trust activity must be reported on the grantor’s final income tax return. The estate will have its own tax reporting responsibility and be required to obtain a TIN.

What is the difference between a grantor trust and a non grantor trust?

Non-grantor trusts are treated as separate entities (like a C-Corporation). But grantors of grantor trusts maintain significant rights to the trust’s assets and income. Because of that, they’re treated as if they are direct owners of the trust assets (like a sole proprietorship).

Does a grantor trust file a tax return?

What happens when the grantor of a grantor trust dies?

Upon the death of the grantor, grantor trust status terminates, and all pre-death trust activity must be reported on the grantor’s final income tax return. Concurrently, the deceased grantor’s estate will come into existence and also be considered a separate taxpayer for income tax purposes.

Who pays the taxes on a grantor trust?

Does a grantor trust need to file a form 1041?

Unlike other trusts, if the entire trust is a grantor trust then the taxpayer is only required to fill in the entity information on Form 1041. The assets held by the trust are normally titled to the trust which informs the IRS that the trust should pickup any applicable income or losses.

The trust may get a distribution deduction for all or part of it. For taxation purposes, trusts can typically be divided into two camps: Grantor trusts, in which all income is taxed to the grantor, regardless of whether the grantor receives distributions from the trust.

Are there alternatives to Form 1041 for grantor trusts?

Described below are alternative methods of reporting and the situations when an alternative reporting method is available. This item also addresses concerns some people have expressed about using these alternatives, particularly with irrevocable grantor trusts (where the trust assets are not includible in the grantor’s taxable estate).

Can a revocable trust be used as a grantor?

This method is most commonly used with revocable trusts which are also grantor trusts for income tax purposes. The second alternative method requires the trust be a reporter of income to the grantor. Under this method, the trust acquires its own taxpayer identification number and furnishes its information to all income payors to the trust.

How to report income from a grantor trust?

This is Stacy Singer, ACTEC Fellow from Chicago. There are several different methods of reporting income tax from grantor trusts. To give us more information on this topic, you will be hearing today from ACTEC Fellow Greg Gadarian from Tucson, Arizona.

Do you need a W-9 for a grantor trust?

The trustee is required to obtain a W-9 to verify grantor’s taxpayer identification number. This method is most commonly used with revocable trusts which are also grantor trusts for income tax purposes. The second alternative method requires the trust be a reporter of income to the grantor.