IRS provides safe harbor to treat rental real estate income as QBI. If all requirements are met, a taxpayer’s rental real estate activities will be treated as a qualified trade or business only for QBID purposes.

Is rental income qualified for Qbi?

Under Internal Revenue Code (IRC) Section 199A, income from rental real estate businesses qualifies as QBI if the business and related rental income qualifies as trade or business income under IRC Section 162. In early 2019, the IRS issued Notice 2019-7.

Can I take Qbi on my rental property?

Notice 2019-07 includes a new safe harbor provision under which a “rental real estate enterprise” (RREE) will be treated as a trade or business under Section 199A of the Internal Revenue Code, thus making it eligible for the QBI deduction.

Is there a qualified business income deduction for 2019?

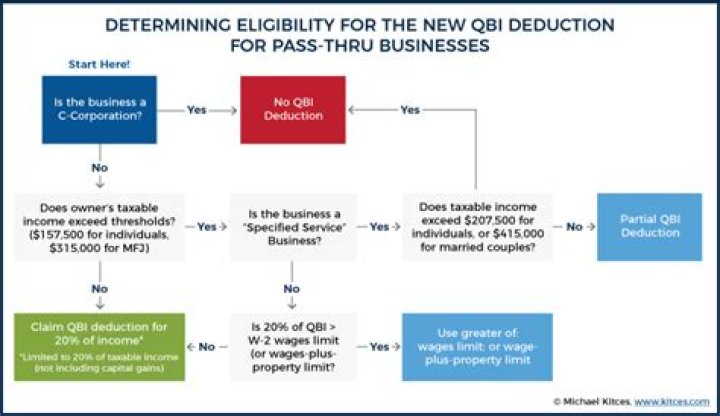

Eligible taxpayers can claim it for the first time on the 2018 federal income tax return they file in 2019. The deduction has two components. This component of the deduction equals 20 percent of QBI from a domestic business operated as a sole proprietorship or through a partnership, S corporation, trust or estate.

Is the rental income from partnership a considered QBI?

The net rental income from Partnership A is deemed QBI. However, the rental income is specified service income because Partnership B is an SSTB and the two partnerships are commonly owned. The IRS issued Notice 2019-07 concurrently with the final QBI regulations.

Is the rental income a business or an investment?

Most notably, landlords who are in business may qualify for the pass-through income tax deduction of up to 20% of their net rental income during 2018 through 2025. Thus, for tax purposes, it’s always better for landlords’ rental activity to be a business, not an investment.

When to use rental income for qualifying purposes?

To determine the amount of rental income from the subject property that can be used for qualifying purposes when the borrower is purchasing or refinancing a two- to four-unit principal residence or one- to four-unit investment property, the lender must consider the following: If the borrower… Then for qualifying purposes…

Who is eligible for the qualified business income deduction?

Qualified Business Income Deduction Many owners of sole proprietorships, partnerships, S corporations and some trusts and estates may be eligible for a qualified business income (QBI) deduction – also called Section 199A – for tax years beginning after December 31, 2017.