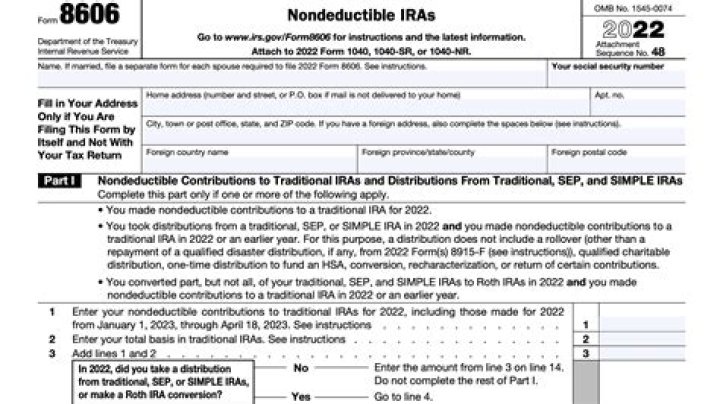

Basically, you must file Form 8606 for every year you contribute after-tax amounts (non-deductible contributions) to your traditional IRA. Conversions from traditional, SEP, or SIMPLE IRAs must also be reported on Form 8606.

What happens if you don t file form 8606?

Failure to file Form 8606 for a distribution could result in the IRA owner (or beneficiary) paying income tax and the additional 10 percent early distribution penalty tax on amounts that should be tax-free. Example: Katlyn made a nondeductible contribution to her traditional IRA for tax year 2017.

How do I add 8606 to TurboTax?

To trigger the 8606 in TurboTax

- Open your return if it isn’t already open.

- Inside TurboTax, search for this exact phrase, including the comma: 8606, nondeductible ira contributions.

- Select the Jump to link in the search results.

- Proceed through the IRA section, answering questions as you go.

Do you have to file IRS Form 8606 every year?

You file one Form 8606 for each year you made a nondeductible contribution. This will establish your basis in the IRA. You would then be eligible to either convert your nondeductible IRAs into Roth IRAs, or you could begin taking distributions from the nondeductible IRAs. And no, according to the IRS, you don’t have to file an amended return.

When to use form 8606 for nondeductible contributions?

Form 8606 for nondeductible contributions Any money you contribute to a traditional IRA that you do not deduct on your tax return is a “nondeductible contribution.” You still must report these contributions on your return, and you use Form 8606 to do so. Reporting them saves you money down the road.

What did Ed Slott claim on form 8606?

Upon audit, he claimed the distribution was basis, despite the fact that he had never filed a Form 8606 or did not have any tax returns to show that a deduction wasn’t taken for certain contributions. Unsurprisingly, the IRS rejected this argument and assessed taxes on the full amount.

Can you file Form 8606 on an unreported basis?

Any unreported basis should be reported on a Form 8606. Even though Form 8606 is normally submitted along with a timely-filed Form 1040, the IRS has indicated that it will process a stand-alone Form 8606, and even one filed beyond the normal 3-year statute of limitations for claiming a refund.