Since the IRS considers any 1099 payment as taxable income, you are required to report your 1099 payment on your tax return. For example, if you earned less than $600 as an independent contractor, the payer does not have to send you a 1099-MISC, but you still have to report the amount as self-employment income.

Who must send 1099-MISC?

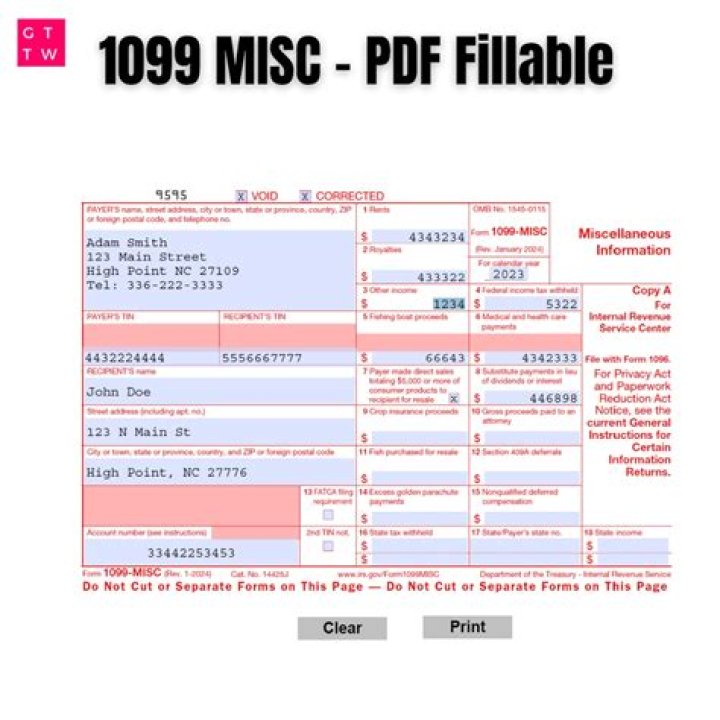

The general rule is that you must issue a Form 1099-MISC to any vendors or sub-contractors you have paid at least $600 in rents, services, prizes and awards, or other income payments in the course of your trade/business in a given tax year (you do not need to issue 1099s for payments made for personal purposes).

Who is required to send 1099-MISC forms?

The entity with the obligation to issue is the broker or insurance company that pays the distribution, provided it is paid directly to the taxpayer. If paid to an intermediary, the intermediary will have the obligation. By far, the broadest reaching of the information returns is Form 1099-MISC, which is used to report miscellaneous income.

What are the penalties for not filing Form 1099 MISC?

Form 1099-Misc needs to be provided for Royalties of $10 or more. If the payer does not file Form 1099-MISC, there is a maximum penalty of $250 per form not filed, up to $500,000 per year. Otherwise for late filings the penalty varies from $30 to $100, depending on how late the filing was.

When is the deadline to file Form 1099-MISC?

If the payer is registered to file electronically with the IRS the deadline for filing with the IRS is March 31. In accordance with the recently passed PATH Act, these deadlines will be changing so the mailing and transmittal are both January 31 moving forward starting with Tax Year 2016. There are several use cases of Form 1099-MISC.

When do I not need to file a form1099 MISC?

If you are a recipient or payee expecting a Form1099-MISC and have not received one, contact the payor. You are not required to file information return (s) if any of the following situations apply: