Reporting the Principal Residence Sale on Your Tax Return For 2017 and later taxation years, Form T2091(IND) Designation of a property as a Principal Residence by an Individual (Other Than a Personal Trust) (T1255 for a deceased taxpayer) must be filed for all principal residence disposals, as indicated on Schedule 3.

What is a T2091 form?

Use Form T2091(IND), Designation of a Property as a Principal Residence by an Individual (Other Than a Personal Trust) to designate a property as a principal residence. You granted someone an option to buy your principal residence, or any part of it.

How does CRA define principal residence?

You designate your home as your principal residence when you sell or are considered to have sold all or part of it. You can designate your home as your principal residence for all the years that you own and use it as your principal residence.

Do both spouses report sale of principal residence CRA?

Note: Only one residence per year can be designated as the principal residence between spouses. If you and your spouse own your home and had a capital gain from its sale, both of you will need to report the gains on your tax return and split it based on your investment in the property.

When do you need to file Form t2091 in Canada?

Canadians need to file Form T2091, however, when selling their principal residence during a year if the property was not their principal residence for every year he/she owned it (e.g., a different property, such as a cottage, was designated as the principal residence for one of the years during the same period of ownership).

When to use form t2091 for principal residence exemption?

The following is a brief overview of Form T2091 which is used to claim the principal residence exemption. The principal residence exemption is an income tax benefit that generally provides an exemption from tax on the capital gain realized when a taxpayer sells a property that is his/her principal residence.

When to use form t2091 when selling your home?

Complete Form T2091 to determine the amount to report. If you had completed form T664 because you sold your primary residence, complete T2091. If you are the authorized person for someone who is deceased, and you sold her primary residence, you will need to complete form T1255.

How is the principal residence exemption calculated in Canada?

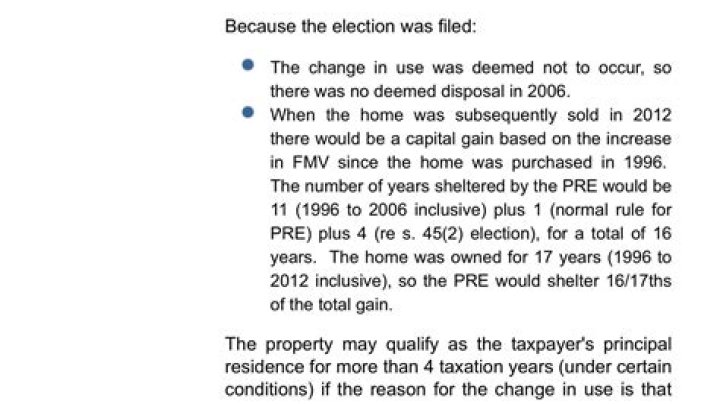

The calculation of the principal residence exemption is based on the following formula: B is 1 + the number of tax years ending after the acquisition date for which the property is designated as the taxpayer’s principal residence and during which he or she was resident in Canada.