Trust beneficiaries must pay taxes on income and other distributions that they receive from the trust, but not on returned principal. IRS forms K-1 and 1041 are required for filing tax returns that receive trust disbursements.

How are trust distributions reported?

IRS Form 1041 is like a Form 1040. This is used to show that the trust is deducting any interest it distributes to beneficiaries from its own taxable income. The trust will also issue a K-1. This IRS form details the distribution, or how much of the distributed money came from principal and how much is interest.

What is a disbursement from a trust?

A trust can be an excellent tool for safely stowing assets that can mature in value for the future benefit of the trust’s beneficiary. When it comes time to remove assets from a trust and deliver them to the beneficiary, this is commonly defined as a trust disbursement.

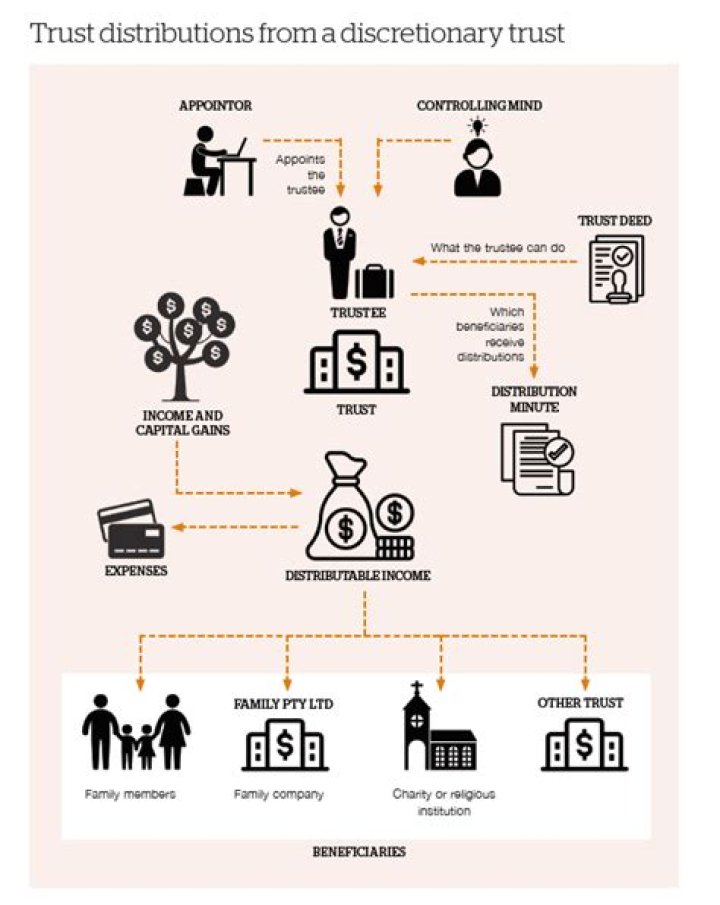

When does a trust fund distribution take place?

You see, the distribution of trust assets to beneficiaries happens when the Trustee, and if applicable, the Co-Trustee, meet all their fiduciary duty. Once the Trustee (s) meet the fiduciary duty, they can complete the trust fund payout. If the trust fund is cash only, trust fund distribution involves writing checks to beneficiaries.

Can a trust be distributed on a staggered basis?

You can have your trust make staggered distributions of trust assets, which means the beneficiaries receive them over time based on rules that you set. For example, the grantor may choose to distribute trust funds on a timed basis, like monthly, or only after certain triggering events, such as when the beneficiary turns 18 or gets married.

Where does a trust distribution go on a 1041?

There actually is no line because if the only distributions were nontaxable, cash distributions and the trust otherwise had no income, there would be no 1041 filing requirement. Regardless, when filing a 1041, the distribution would wind up on Line 10 of Schedule B. The distribution would not, however, appear on the K-1.

How are trust funds disbursed after death?

Then disbursement is made based on the grantor’s wishes when he/she set up the trust. Distribution of trust assets can be made in a lump sum, as a percentage of trust principal or income, or as payment for medical expenses, school fees, etc. If the trust has only one named beneficiary, distribution of trust funds after death is fast and easy.