A Credit Carryforward, also called a Carryover, allows you to apply a leftover amount of a previous year tax credit to a current year tax return. The eFile.com software will allow you to enter the carryover amount from the previous tax year.

Is there a cap on dependents for taxes?

Although there are limits to specific dependent credits, there’s no maximum number of dependent exemptions you can claim. If a person meets the requirements for a qualifying child or relative, you can claim him or her as a dependent. You can do this as a single filer and regardless of your filing status.

How long can you carry over tax credits?

Carryback and Carryover of Unused Credit You can carry back for one year and then carry forward for 10 years the unused foreign tax. For more information on this topic, see Publication 514, Foreign Tax Credit for Individuals.

When do you have to carry over tax deductions?

If you experience a loss, you may be able to carry over a deduction for your loss into future tax years. When your deductions for a tax year are more than your income for the same year, you might have an NOL.

Who are the dependents on your income tax return?

In order to claim someone as your dependent, the person must be: Either your qualifying child or qualifying relative; A U.S. citizen, U.S. resident, U.S. national or a resident of Canada or Mexico; Unmarried or, if married, not filing a joint return or only filing a joint return to claim a refund of income tax withheld or estimated tax paid.

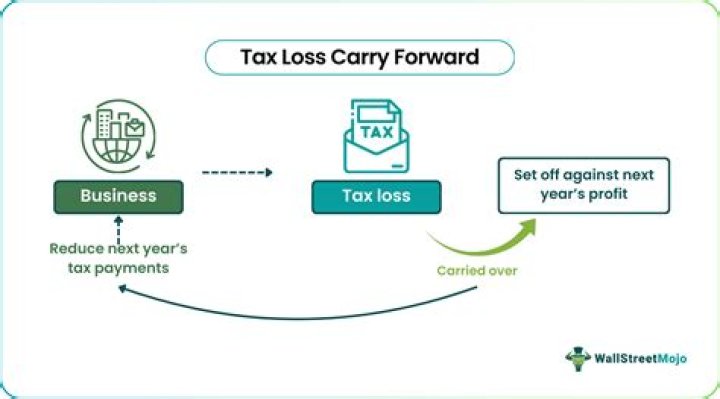

Can a loss be carried over to the next tax year?

If you experience a loss, you may be able to carry over a deduction for your loss into future tax years. When your deductions for a tax year are more than your income for the same year, you might have an NOL. Any NOL you may have could potentially be carried over as a deduction from your income in previous tax years.

When to use carry forward tax deductions and credits?

For the Non-Business Energy Property Credit, the carryforward period is 20 years. Bottom line Along with IRS rules for when certain deductions or credits can be applied to subsequent tax years, Colabella says that using a carryforward should depend on “whether or not the taxpayer achieves a better tax result.”