Charitable remainder annuity trusts (CRATs) distribute a fixed annuity amount each year, and additional contributions are not allowed.

How do I set up a charitable remainder trust?

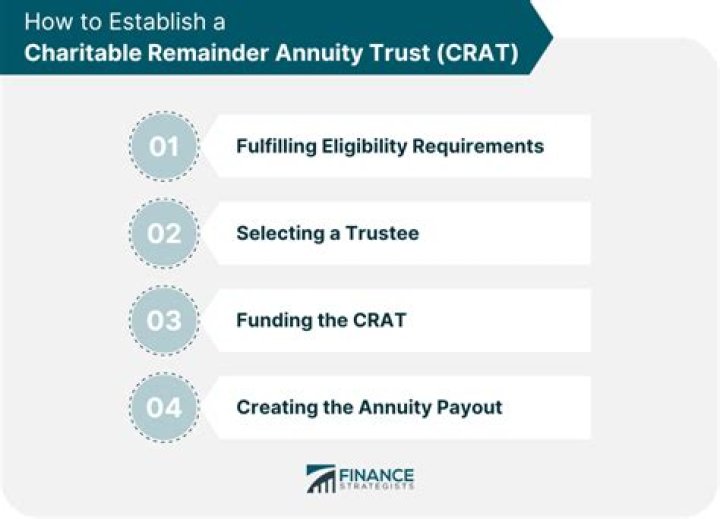

How to Set up a Charitable Remainder Trust

- Create a Charitable Remainder Trust.

- Check with the IRS that the charity you want to benefit is approved.

- Transfer assets into the Trust.

- Name the charity as Trustee.

- Create a provision that states who the lead beneficiary is – remember, this can be yourself or someone else.

Can 5227 be E filed?

Form 5227, Split-Interest Trust Information Return, cannot be e-filed. The form is available in the 1041 fiduciary return by completing applicable screens on the 5227 tab. The presence of a Form 5227 does not prevent e-filing a 1041, but the 5227 is not transmitted with the 1041.

Can you add to a CRUT?

The Charitable Remainder Unitrust or CRUT pays an income stream to the taxpayer that is based on a taxpayer chosen percentage of the fair market value of the CRUT-owned assets every year. Unlike with the CRAT, the taxpayer can make additional contributions to a CRUT.

How long does a charitable remainder trust last?

A CRT may last for the Lead Beneficiaries’ joint lives or for a term of years (the term may not exceed 20 years). In addition, the actuarial value of the CRT remainder left to charity must be least 10% of the initial CRT value, determined at time of funding.

What are the tax benefits of a charitable remainder trust?

Benefits of a Charitable Remainder Trust

- Convert an appreciated asset into lifetime income.

- Reduce your current income taxes with charitable income tax deduction.

- Pay no capital gains tax when the asset is sold.

- Reduce or eliminate your estate taxes.

- Gain protection from creditors for the gifted asset.

What is the penalty for filing Form 5227 late?

The Pension Protection Act altered the penalties for failure to file Form 5227 as follows: The penalty for failure to file is $20 for each day the failure continues, with a maximum of $10,000 for any one return.

Who must file Form 5227?

All charitable remainder trusts described in section 664 must file Form 5227. All pooled income funds described in section 642(c)(5) and all other trusts such as charitable lead trusts that meet the definition of a split-interest trust under section 4947(a)(2) must file Form 5227 unless the Exception next applies.

How does a charitable remainder annuity trust work?

Charitable remainder annuity trusts (CRATs) distribute a fixed annuity amount each year, and additional contributions are not allowed. Charitable remainder unitrusts (CRUTs) distribute a fixed percentage based on the balance of the trust assets (revalued annually), and additional contributions can be made.

What are the different types of remainder trusts?

Charitable remainder trusts can be structured in numerous ways. The two basic categories are charitable remainder annuity trusts (CRATs) and charitable remainder unitrusts (CRUTs). The primary difference between the two basic categories is how the income payment is calculated.

What happens to the assets of a charitable trust?

the remaining trust assets upon termination. Charitable remainder trusts can be either annuity trusts or unitrusts, depending on the method used to calculate the payment amounts.

Is the income from a charitable remainder trust tax exempt?

Tax exempt: The CRT’s investment income is exempt from tax. This makes the CRT a good option for asset diversification. You may consider donating low-basis assets to the trust so that when sold, no income tax is generated to you and you eliminate the capital gains tax on the sale of the asset.