Specifically, you have until each year’s tax deadline to make your IRA contributions. For 2018, this means you can make your contributions from January 1, 2018 through April 15, 2019. Similarly, 2017 IRA contributions can be made until April 17, 2018, the day that 2017 tax returns are due.

How late can I make an IRA contribution for 2018?

The deadline for 2018 traditional and Roth contributions for most taxpayers is April 15, 2019 (April 17 for those in Maine and Massachusetts). There are some ground rules. You must have enough 2018 earned income (from jobs, self-employment or alimony) to equal or exceed your IRA contributions for the tax year.

Are IRA contributions based on previous year income?

Only earned income can be contributed to a Roth IRA. You can contribute to a Roth IRA only if your income is less than a certain amount. The maximum contribution for 2021 is $6,000; if you’re age 50 or over, it is $7,000.

Is it too late to contribute to an IRA for 2019?

You can contribute to either a traditional or Roth IRA until the April 15th due date, not including extensions. Be sure to tell the IRA trustee that the contribution is for 2019. Otherwise, the trustee may report the contribution as being for 2020 when they get your funds.

When do you have to contribute to an IRA in 2018?

Finally, your contributions must be made in a timely manner. For IRA purposes, this means that you can contribute during the calendar year itself, or during the next calendar year before the tax deadline passes. In 2018, this means your contributions must be made between Jan. 1, 2018 and April 15, 2019.

Do you qualify for an IRA deduction in 2018?

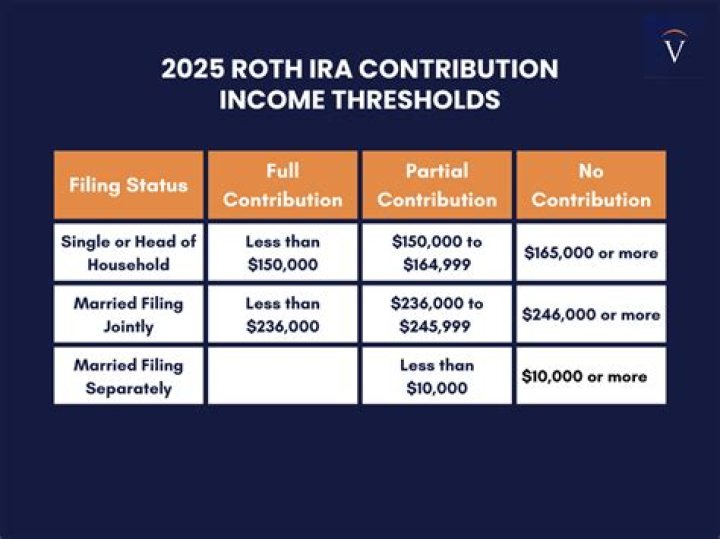

Income limitations: Are you eligible to participate in an employer’s retirement plan? 2018 Tax Filing Status Full Contribution Limit Partial Contribution Phaseout Single or head of household $63,000 $73,000 Married filing jointly $101,000 $121,000 Married filing separately ( if you lived $0 $10,000

What makes you eligible to contribute to an IRA?

In addition, you need to be eligible to contribute to an IRA at all, which means that you have earned income, which includes wages, salaries, tips, bonuses, etc. In other words, if all of your income comes from investments or from a business you don’t have an active role in, it doesn’t count for IRA eligibility purposes.

Is there a limit to how much you can contribute to an IRA?

Contributions to an IRA may be eligible for a tax deduction, up to the annual contribution limit, which is $5,500 for the 2018 tax year or $6,500 if you’re 50 or older.