Expats required to file IRS form 5472, should file this form along with the company’s yearly tax return. When there are several foreign owners that each own over 25% of the corporation, a separate form 5472 is filed for each one. Also, you cannot file the form electronically.

Who is required to file a 5472?

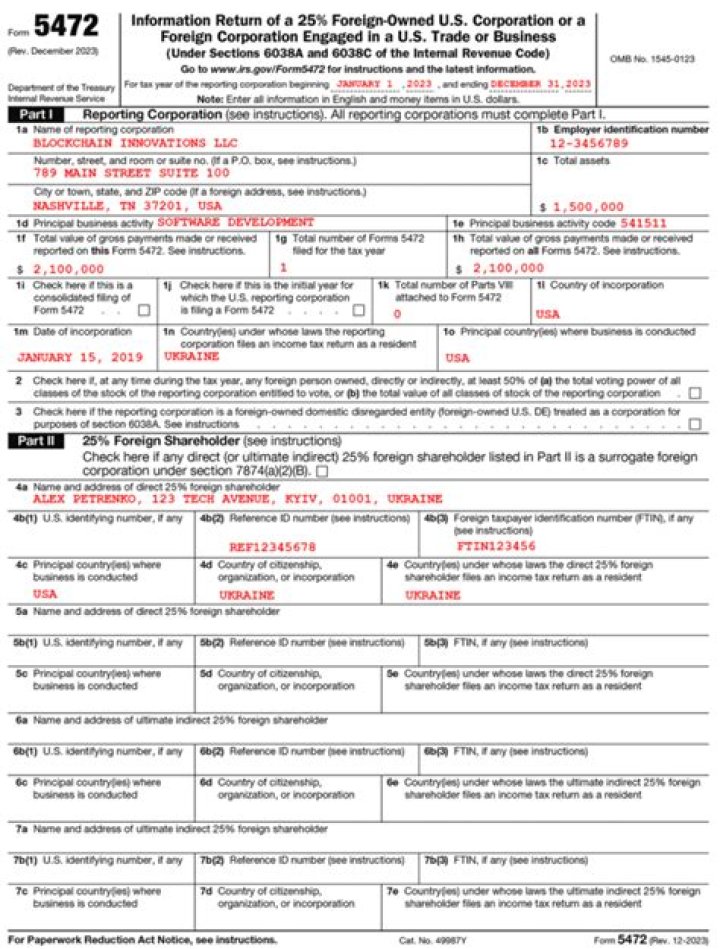

Who has to file? A U.S. corporation with 25% or more foreign ownership, or foreign corporations that do business or trade in the U.S. are required to file IRS Form 5472. You must report the existence of all related parties in Form 5472 as well, and fill out a separate form for each foreign owner.

What do you need to know about the 5472 form?

The 5472 form is an international tax form that is used by foreign person’s to report an interest in, or ownership over a U.S. company or subsidiary. Technically, the form is referred to as the: Information Return of a 25% Foreign-Owned U.S. Corporation or a Foreign Corporation Engaged in a U.S. Trade or Business.

Can a Consolidated Corporation file a Form 5472?

FORM 5472 CONSOLIDATED REPORTING •If a reporting corporation is a member of an affiliated group filing a consolidated U.S. Federal income tax return then it can satisfy the requirements by filing a consolidated Form 5472.

When to use Form 5472 for IRC 6038a?

“Use Form 5472 to provide information required under sections 6038A and 6038C when reportable transactions occur during the tax year of a reporting corporation with a foreign or domestic related party.” What is IRC 6038A?

What is the penalty for not filing Form 5472?

When a person does not file the Form 5472 timely, they may be subject to fines and penalties. “A penalty of $25,000 will be assessed on any reporting corporation that fails to file Form 5472 when due and in the manner prescribed. The penalty also applies for failure to maintain records as required by Regulations section 1.6038A-3.