E-Filing: You can e-file the return in which you generate Form 1045, but Form 1045 does not e-file with the return, nor may it be e-filed separately. Preparers should paper file Form 1045 the same way as they would paper file Form 1040 for the same taxpayer.

What is the purpose of Form 1045?

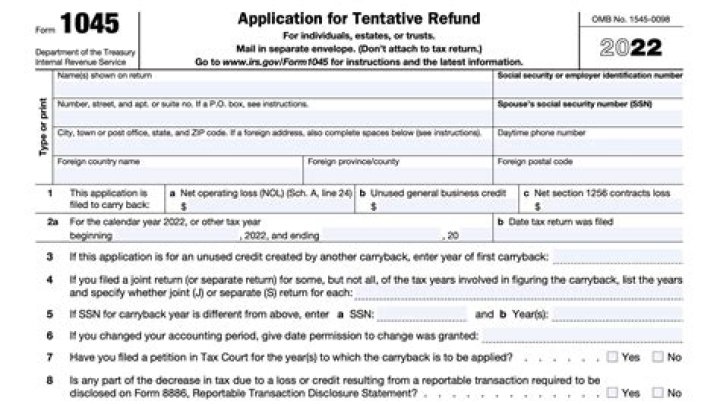

An individual, estate, or trust files Form 1045 to apply for a quick tax refund resulting from: The carryback of an NOL. The carryback of an unused general business credit. The carryback of a net section 1256 contracts loss.

What is a section 965 A inclusion?

Section 965 allows U.S. shareholders to reduce the amount of the income inclusion based on deficits in earnings and profits with respect to other specified foreign corporations.

What to do if you get carryback on Form 1045?

If a taxpayer files a late Form 1139 or Form 1045, as applicable, to apply for a tentative refund from the carryback of an NOL, the Form 1139 or Form 1045 will be rejected, and the taxpayer will be instructed to file amended returns for each applicable tax year in the five-year carryback period.

How to calculate Nol carryover on Form 1045?

If the taxable income (Line 15) in the “Before carryback” column is not greater than the NOL deduction being carried back, proceed with the steps below to complete Form 1045 Schedule B – NOL Carryover to calculate the amount of loss remaining to carry to the following year.

Can you file Form 1045 for loss you carry back to section 965?

Because of the changes in the NOL rules under the CARES Act, you may now file Form 1045 for a 2019 loss you carry back to a section 965 year. If you carry back your NOL to a section 965 year in the 5-year carryback period, you are deemed to have made an elec- tion under section 965(n) for the NOL being car- ried back.

When do I need to file Form 1045?

If there are NOLs being carried forward from multiple years, you must calculate each amount separately and then add them together to enter on Line 8 of Schedule 1 (Form 1040). Form 1045. Generally, you must file Form 1045 on or after the date you file your tax return for the NOL year, but not later than one year after the end of the NOL year.