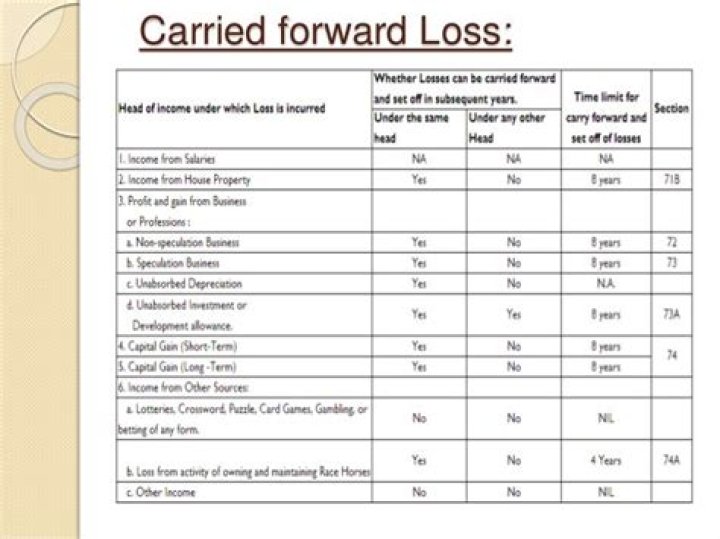

In the subsequent years(s) such loss can be adjusted only against income chargeable to tax under the head “Income from house property”. Such loss can be carried forward for eight years immediately succeeding the year in which the loss is incurred. [As amended by Finance Act, 2020]

When to adjust loss under one head of income?

If in any year, the taxpayer has incurred loss under one head of income and is having income under other head of income, then he can adjust the loss from one head. [As amended by Finance (No. 2) Act, 2019] against income from other head, E.g., Loss under the head of house property to be adjusted against salary income.

Can a loss be set off against any other income?

2) Loss from speculative business cannot be set off against any other income. However, non-speculative business loss can be set off against income from speculative business. 3) Loss under head “Capital gains” cannot be set off against income under other heads of income.

Can a short-term loss be adjusted against a long-term gain?

Short-term capital loss can be adjusted against long-term capital gains as well as short-term capital gains. Such loss can be carried forward for eight years immediately succeeding the year in which the loss is incurred.

Is there a limit on the amount of loss relief you can claim?

There’s a limit on the total amount of Income Tax reliefs that you may claim for deduction from total income for a tax year. Loss relief is one of the reliefs affected. The limit is the higher of £50,000 and 25% of the adjusted total income of the year. See Helpsheet 204 if you think you may be affected by this.

When to carry back a Section 1256 loss?

60 percent of the amount so allowed shall be treated as a long-term capital loss from section 1256 contracts. The entire amount of the net section 1256 contracts loss for any taxable year shall be carried to the earliest of the taxable years to which such loss may be carried back under paragraph (1).

How to file and claim losses claiming capital losses?

How to File and Claim Losses Claiming capital losses requires filing IRS Form 8949, “Sales and Other Dispositions of Capital Assets,” with your tax return, in addition to Schedule D, “Capital Gains and Losses.”