The IRS is fine with parents and grandparents (and anyone else) giving someone the money to contribute to a Roth IRA. In 2019 the maximum contribution rises to $6,000. The only catch is that the recipient must have earned income that is at least equal to the amount contributed.

How much can I contribute to my son’s Roth IRA?

The Roth IRA contribution limit is $6,000 in 2021 ($7,000 if age 50 or older), or the total of earned income for the year, whichever is less. If a child earns $2,000 baby-sitting in 2020, he or she can contribute up to $2,000 to a Roth IRA.

Can my child inherit my Roth IRA?

If you have a Roth IRA and don’t designate a beneficiary, it could get lumped into your total estate and divided according to the laws in your state. Your spouse or children may ultimately end up with your money, but they won’t have access to the same tax benefits as if you had named them as beneficiaries.

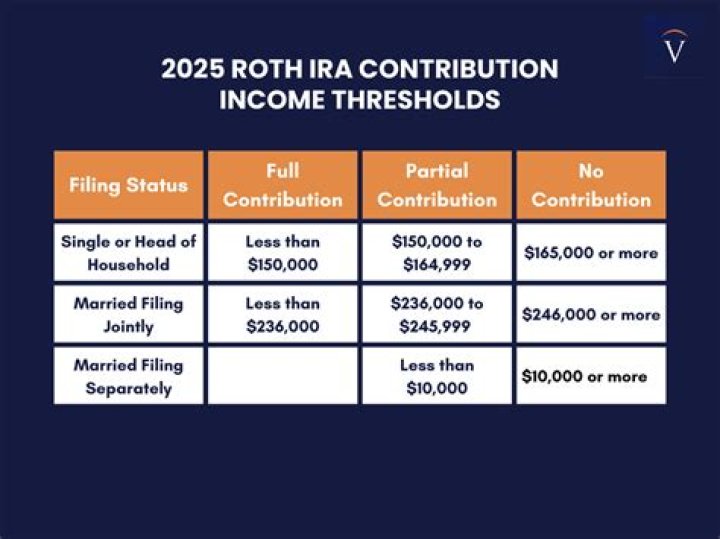

Are there income limits to contribute to a Roth IRA?

Investment income does not qualify. The contribution limits on IRAs change periodically based on inflation. For 2020 and 2021, workers can contribute up to $6,000 a year to a Roth IRA ($7,000 for those 50 or older). But the contribution can only be as large as the individual’s earned income.

Are there limits on contributions to a Charles Schwab Roth IRA?

Roth IRA Contribution Limits | Charles Schwab IRS Tax Relief: Federal tax deadlines, payments and IRA contributions for 2020 have been extended to May 17, 2021. Furthermore, residents and businesses affected by severe winter storms in Texas, Oklahoma, and Louisiana have been extended to June 15, 2021. 2020-2021 Roth IRA Contribution Limits

How much can a teenager contribute to a Roth IRA?

For 2020 and 2021, workers can contribute up to $6,000 a year to a Roth IRA ($7,000 for those 50 or older). But the contribution can only be as large as the individual’s earned income. If a teen earned $4,000 during the year, that is the most they can contribute. 1

How old do you have to be to contribute to Roth IRA?

The 5-year rule applies regardless of your age when you opened the account. If you are 58 years old when you make your first contribution, for example, you still have to wait until age 63 to avoid taxes. The clock starts ticking on Jan. 1 of the year you made your first contribution to any Roth.