They give up ownership of the property funded into it, so these assets aren’t included in the estate for estate tax purposes when the trustmaker dies. Irrevocable trusts file their own tax returns, and they’re not subject to estate taxes, because the trust itself is designed to live on after the trustmaker dies.

Do you pay taxes on trusts?

Trusts are subject to different taxation than ordinary investment accounts. Trust beneficiaries must pay taxes on income and other distributions that they receive from the trust, but not on returned principal. IRS forms K-1 and 1041 are required for filing tax returns that receive trust disbursements.

Are grantor trusts subject to Illinois replacement tax?

A Grantor Trust is a trust whose existence is ignored for U.S. and Illinois income tax purposes. A Grantor Trust does not file the federal Form 1041 or Form IL-1041, Fiduciary Income and Replacement Tax Return.

Do you have to pay income tax on a trust in Illinois?

Illinois law wasn’t referenced in the trust instrument. The Illinois Department of Revenue (the “IDR”) determined that the trust was a resident trust and that, as such, the trust should continue to be subject to Illinois income tax.

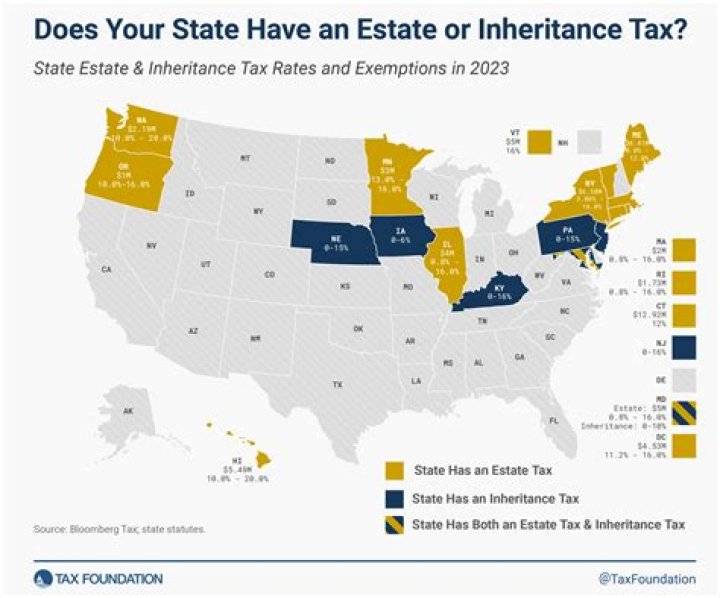

Do you have to pay estate tax in Illinois?

When someone passes away, if he or she owns assets with a dollar value in excess of the state and/or federal estate tax exemption amounts, the amount of assets over and above the exemption amounts will be subject to state and federal estate tax respectively. The Illinois estate tax exemption is $4 million.

Can a revocable living trust be used to avoid estate tax?

Revocable Living Trusts can be used to allow married couples to take advantage of one another’s estate tax exemptions, essentially raising the threshold at which the couple has to worry about Illinois estate tax from $4 million to $8 million in assets.

What kind of tax return do you need to file in Illinois?

You must file Form IL-1041, Fiduciary Income and Replacement Tax Return, if you are a fiduciary of a trust or an estate, and the trust or estate: has net income or loss as defined under the Illinois Income Tax Act (IITA) allocable to Illinois, regardless of any deduction for distributions to beneficiaries;