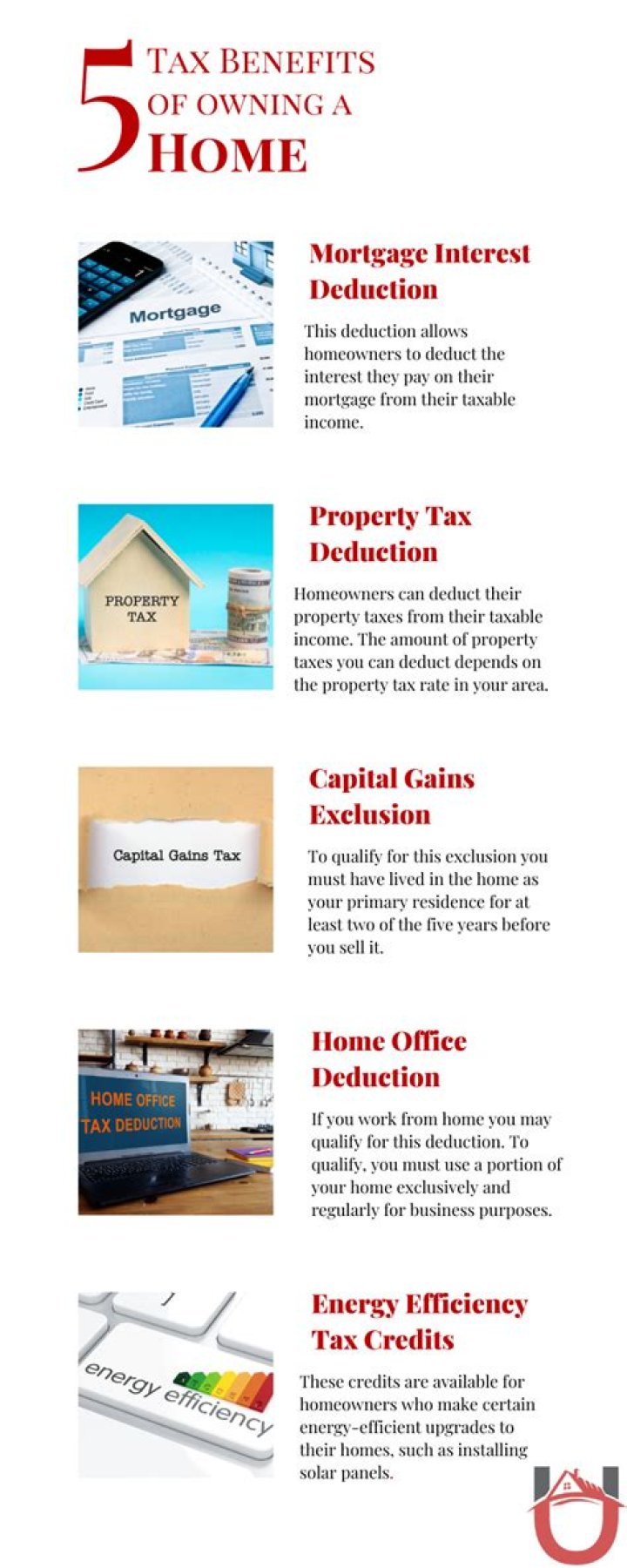

The following can be eligible for a tax deduction: Your property taxes. The mortgage interest on your primary residence, as well as on a second residence. The interest on up to $100,000 borrowed on a home equity loan or home equity line of credit, regardless of the reason for the loan (for tax years prior to 2018 only).

Are there any tax deductions for people over 65?

In 2013, the tax code was changed so that people 65 and under could only deduct medical and dental expenses in excess of 10 percent of their gross adjusted income. (So if you made $50,000, you could deduct any medical costs over $5,000.) But over the age of 65, you’re allowed to deduct any costs over 7.5 percent.

When do you get a tax deduction for retirement?

Contributions to traditional IRAs are tax deductible (subject to income limits if you have another retirement plan. However, withdrawals made after retirement qualifies as taxable income. In contrast, contributions to Roth IRAs are not deductible, but you pay no income tax on withdrawals you make after age 59½.

What are the largest deductions for retired people?

Medical and dental expenses are often one of the largest expenses for retired people. Fortunately, some of these expenses are deductible if you itemize your personal deductions.

What kind of home improvements can I deduct on my taxes?

For example, you can install entrance ramps, create modified bathrooms, lower cabinets, widen doors, add handrails, and create special doors. These are all improvements that can be deducted through the medical expense’s deduction.

What do you need to know about tax deductions?

• The taxpayer must have an area of their home, which is used exclusively for this purpose. For example, taxpayers who meet clients at their home in their dining room would not qualify. A separate office, which is used specifically for the taxpayer’s work, needs to be maintained in order to qualify for the deduction.

What are the tax deductions for a home equity line of credit?

The interest on up to $100,000 borrowed on a home equity loan or home equity line of credit, regardless of the reason for the loan (for tax years prior to 2018 only). Points that you paid when you purchased the house (or those that you convinced the seller to pay for you). Home improvements required for medical care.