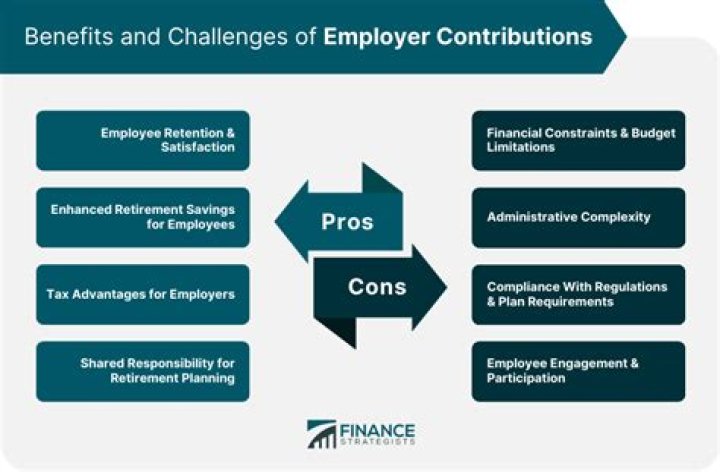

Employer contributions are deductible on the employer’s federal income tax return to the extent that the contributions do not exceed the limitations described in section 404 of the Internal Revenue Code. Elective deferrals and investment gains are not currently taxed and enjoy tax deferral until distribution.

What is the maximum amount of the credit for small employer pension plan start up costs in 2020?

The credit equals 5 percent (5%) of the cost to set up and administer the pan, up to a maximum of $550 per year for each of the first 3 years of the plan. You can choose to start claiming the credit in the tax year before the tax year in which the plan becomes effective.

Do you have to put your retirement plan on your taxes?

You have to pay income tax on your pension and on withdrawals from any tax-deferred investments—such as traditional IRAs, 401(k)s, 403(b)s and similar retirement plans, and tax-deferred annuities—in the year you take the money. The taxes that are due reduce the amount you have left to spend.

Is employer match tax deductible?

In short, the answer to the question “Can an employer deduct matched contributions to retirement plans?” is a resounding “yes.” Even some of the administrative fees of managing a 401(k) plan can be tax-deductible. Putting extra funds into a matched 401(k) provides tax benefits to both you and your employees.

How does the saver’s tax credit work?

The saver’s credit is worth up to $1,000 ($2,000 if married filing jointly). “The saver’s credit is worth up to $1,000, or $2,000 for those married filing jointly.” The value of the saver’s credit is calculated based on your contributions to a traditional or Roth IRA, 401(k), SIMPLE IRA, SARSEP, 403(b) or 457(b) plan.

How much retirement can you deduct from taxes?

For 2020 and 2021, there’s a $6,000 limit on taxable contributions to retirement plans. Those aged 50 or over can contribute another $1,000. In the eyes of the IRS, your contribution to a traditional IRA reduces your taxable income by that amount and, thus, reduces the amount you owe in taxes.

Is there a tax credit for retirement plans?

Retirement Plans Startup Costs Tax Credit Eligible employers may be able to claim a tax credit of up to $5,000, for three years, for the ordinary and necessary costs of starting a SEP, SIMPLE IRA or qualified plan (like a 401 (k) plan.) A tax credit reduces the amount of taxes you may owe on a dollar-for-dollar basis.

How to claim the retirement plan startup costs tax credit?

Retirement Plans Startup Costs Tax Credit. You may be able to claim a tax credit for some of the ordinary and necessary costs of starting a SEP, SIMPLE IRA or qualified plan. A tax credit reduces the amount of taxes you may owe on a dollar-for-dollar basis. If you qualify, you may claim the credit using Form 8881,…

How much are 401k contributions tax deductible for employers?

Make a smart compensation decision Employee Income After-Tax Employer Net Cost Employer Net Cost Employer Net Cost $3,000.00 Increased Pay $3,000.00 Increased Payroll ($750.00) Taxes @ 25% $229.50 FICA @ 7.65% ($807.38) Tax Deduction @ 25% $2,250.00 Net Paycheck $2,422.12 Net Cost

When to claim tax credit on 401K contributions?

Although the credit may be claimed for each of the first three years of the plan, an employer may choose to start claiming the credit in the tax year prior to the plan becoming effective.