For Contracts That Are Not Tax Qualified: We are required to report to the Internal Revenue Service on Form 1099-LTC the gross amount of long-term care benefits issued under your insurance contract, on a yearly basis. Since your contract is not tax qualified, some or all of your benefits may be taxable.

Are LTC payouts taxable?

In general, the income from a long-term care insurance policy is non-taxable, and the premiums paid to buy the insurance are tax deductible.

What LTC benefits are taxable?

LTA/LTC is a tax break that can be availed by an employee for travel of self and family members anywhere in India. The leave encashment portion is taxable in the hands of an employee. The amount of LTA that can be claimed as tax-exempt is limited to the actual fare of rail/air/bus travel.

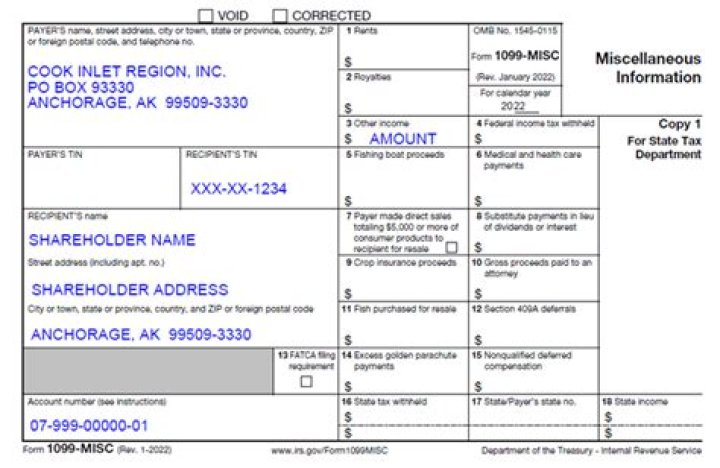

When to include 1099-ltc on your tax return?

You should receive a 1099-LTC if during the previous year you received long-term care benefits, including accelerated death benefits. It helps to understand a few terms before you include your 1099-LTC with your tax return.

How is cash surrender value of life insurance taxable?

If the CSV is more than the premiums and you surrender the policy (cancel it), the excess is earnings and taxable income. For example, if you paid $1,000 in policy premiums for 20 years and you cash in the policy and receive $30,000, you’ll pay ordinary income tax on $10,000 in earnings.

How to calculate taxable amount on a 1099-R for life insurance?

You will, however, receive a 1099-R reporting a $50,000 distribution paid to you by your life insurance company. The 1099 will report the distribution amount of $50,000 and also report that $0 is taxable. More specifically, Box 1 of the 1099-R will show the $50,000 distribution.

How to report a foreign life insurance policy surrender?

I your case, as it is a foreign life insurance policy, it is possible that premiums were paid in a currency other than US dollars. If that is the case do the above suggested calculation in the foreign currency and convert the resulting taxable amount to US dollars using the exchange rate on the date you constructively received the proceeds.